Syndax Pharmaceuticals

10-07-2025 | NASDAQ: SNDX | Price: $16.45 | Market Cap: $1.41B

preface

Biotech is a graveyard of ambition. PowerPoint dreams meet Phase 3 reality… and most of the sector burns through cash faster than it builds conviction. The game rewards clarity, not charisma…Expertise, not ego. Meaningful innovation is not just discovery, it is endurance. Turning a molecule into a market is where real separation happens. Syndax is one of the few small caps showing it can do both, building while executing and innovating while scaling.

At 24k, we do not chase novelty. Syndax fits that frame with focused science, real revenue, and catalysts that actually matter. I believe it is undervalued and dynamic, positioned at the intersection of scientific proof and commercial execution. Few biotechs of its size show this level of traction with this degree of discipline.

Source: ThePharmaLetter

thesis

Syndax sits in a rare lane, a mid-stage biotech with two commercial launches and a credible line to profitability. Revuforj and Niktimvo are scaling, not selling hope. If the October readout hits, Revuforj becomes a front-runner in a $5B menin class. The setup is simple: Street models still treat this as one-off launch risk. The reality is, they now have two growth engines, both early in curve, both de-risked.

If the FDA clears the NPM1 label expansion for Revuforj, the addressable patient pool more than doubles. At that point, consensus revenue targets will need to reset sharply higher. With current Street estimates projecting around $250–300M in combined 2026 revenue, even a conservative re-rate to 7–8x sales brings valuation into the $30–$40 zone. That assumes no change in expense guidance — which management has held steady through two launches.

On the operating side, Syndax is already behaving like a company priced for much larger scale. Quarterly growth trends are clean, cash runway extends through 2026, and the co-promotion model with Incyte cushions burn. If Revuforj’s October data lands as expected, multiple expansion will follow naturally — both from higher sales visibility and a structural shift in perception. This moves Syndax from “story stock” to early-stage operator.

No position currently, long biased.

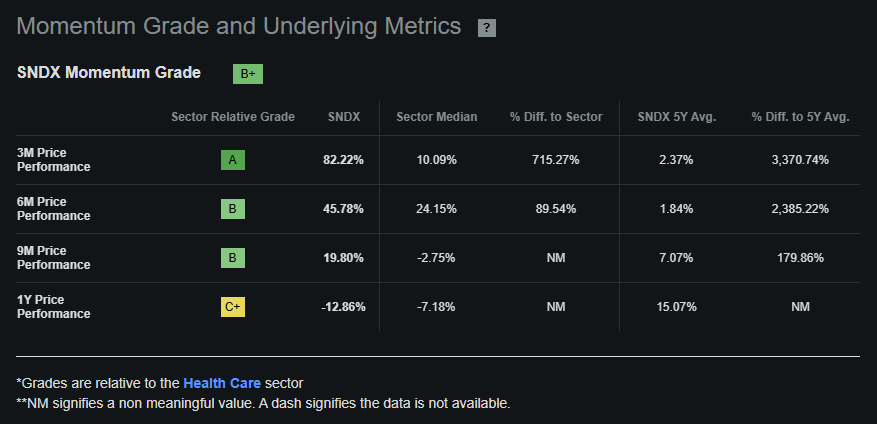

momentum View

Syndax’s recent price action shows strength that the broader sector has yet to recognize. Over the past three to six months, SNDX has outperformed the healthcare median by more than 700% in short-term momentum and nearly 90% in mid-term relative strength. (Below)

Source: Seeking Alpha Premium

SNDX has built a clean uptrend off the July base, reclaiming the 20-, 50-, and 200-day moving averages with rising volume. The stock has respected its short-term trendline since August, confirming steady accumulation rather than speculative spikes. RSI near 62 shows constructive momentum without exhaustion, suggesting room to push through the $17 resistance zone.

A breakout and hold above $17.00 could open a technical path toward $19–$21 in the near term, with $24–$26 as the next structural range if the October catalyst lands. The chart supports the broader thesis: controlled momentum, clear higher lows, and rising participation ahead of a binary event. (Below)

Source: Finviz Elite

products / pipeline

revuforj (revumenib)

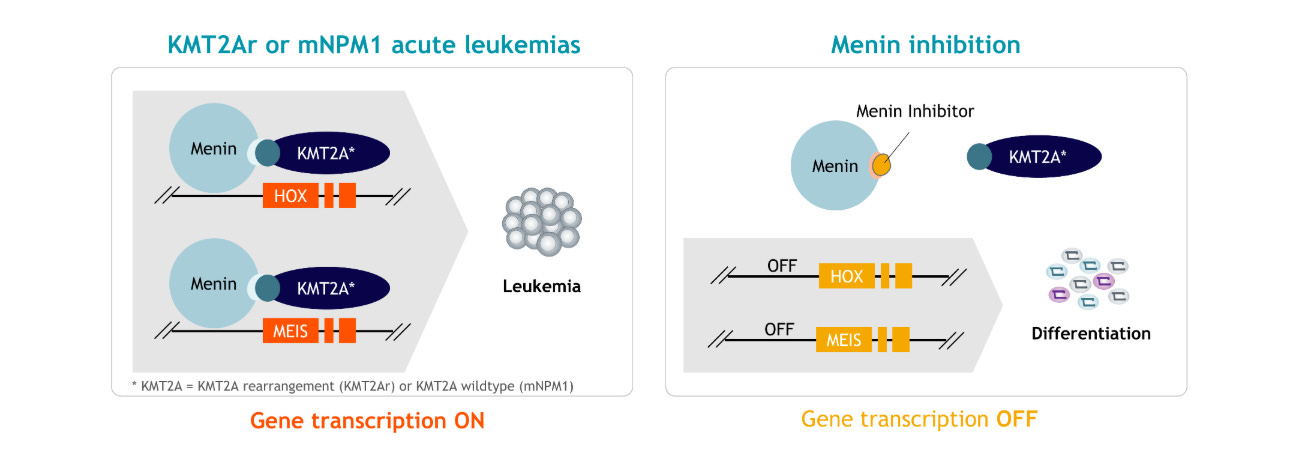

Approved for relapsed and refractory acute leukemia with KMT2A rearrangements. it blocks menin, a protein that helps leukemia cells grow. The next step is a label expansion for NPM1 mutant AML, which could double its market reach. menin inhibition is one of the few precision oncology approaches showing consistent results across genetic subtypes.

Mechanism of action: menin inhibitors like revuforj block the interaction between menin and KMT2A/NPM1, shutting off cancer-driving gene transcription and allowing leukemic cells to differentiate.(Below)

Source: Syndax

niktimvo (axatilimab)

Launched for chronic graft versus host disease, a serious immune reaction that can follow bone marrow transplants. it targets CSF1R to calm the immune system and reduce inflammation. Partnered with incyte, giving syndax shared costs and steady royalty income. Expansion plans in first line cGVHD and idiopathic pulmonary fibrosis, with mid stage data expected in 2026, add growth potential without stretching spending.

Mechanism of action: axatilimab blocks the CSF-1 receptor on monocytes and macrophages, reducing the signals that drive fibrosis and inflammation in chronic graft-versus-host disease. (Below)

Source: Syndax

key data

revuforj q2 rev $28.6M (+43% q/q)

niktimvo $36.2M first full US quarter

total rev $38M, beat est. by around $11M

peak sales est. $1B+ each asset

stifel price target $44 | citi price target $51

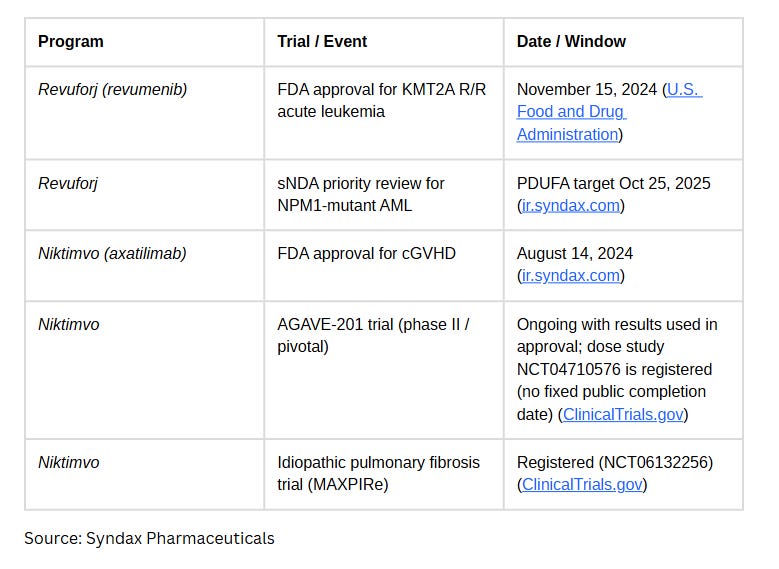

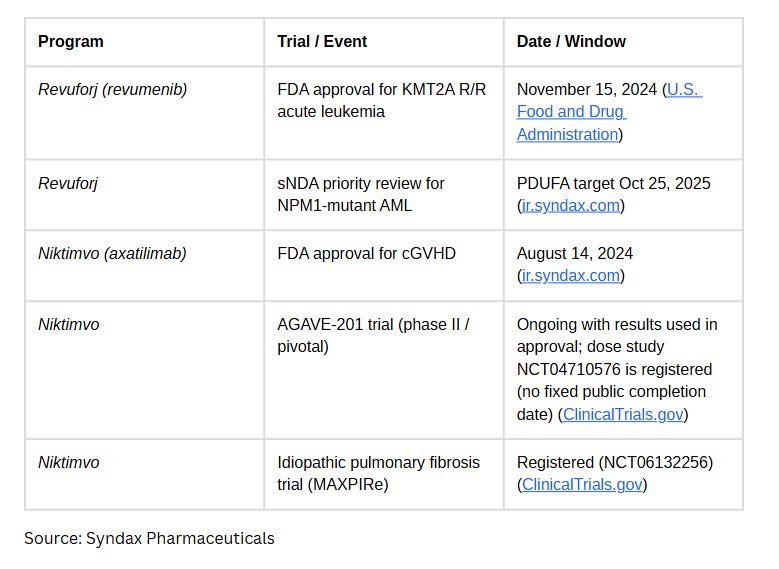

oct 25 2025: major fda decision for revuforj NPM1 AML expansion

52w range $8.58–22.50 | fwd eps –3.13

conclusion

Syndax is moving from small-cap speculation to real execution. Two products in market, both scaling faster than expected, and a near-term fda decision that could reshape its growth curve pretty quick. This isn’t the usual binary biotech bet anymore, it’s a company in transition, building a base of recurring revenue with optionality and innovation on top.

The setup into October looks clean: limited downside if the label expansion drags, asymmetric upside if it lands. Management’s discipline on spend and consistent delivery signal that they’re not guessing their way through commercialization, they’re operating.

The market still prices syndax like a one-shot story, imo it’s becoming clear, that it is not.

disclaimer: this report is for informational and educational purposes only. it is not financial advice, a recommendation, or a solicitation to buy or sell any security. all opinions expressed are those of 24k research at the time of writing and are subject to change without notice. investors should conduct their own due diligence and consult a qualified financial advisor before making investment decisions.