OKLO Inc

2025-09-21

Preface & Background

OKLO 0.00%↑ Oklo Inc, founded in 2013 by Jacob DeWitte and Caroline Cochran, is a developer of advanced small-scale fast neutron reactors and nuclear fuel recycling technologies.

Its mission is clean, reliable, and affordable energy using its Aurora reactor line, which aims for inherent safety, long refueling intervals, and using recycled nuclear waste / advanced fuel cycles.

Oklo went public in mid-2024 through a SPAC backed by well-known tech and venture investors, including Hydrazine Capital. Its Aurora reactor has made early regulatory progress, securing a site use permit and fuel allocation from Idaho National Lab, with further permissions in process. That said, the company’s first license application was rejected by the U.S. Nuclear Regulatory Commission (NRC) in 2022 for incomplete information… not safety issues. Oklo can reapply, but licensing remains a critical hurdle until fully approved.

Strategically, the company is targeting high-demand power users, the likes of data centers, AI infrastructure, remote communities, and defense installations — under long-term supply agreements. Several partnerships and MOUs with credible names are already in place.

Financially, however, Oklo is still in the early stage. The company has yet to generate operating revenue and continues to post sizable losses. In Q2 2025, it reported a net loss of $24.7 million on operating expenses of $28 million, underscoring how far it remains from positive cash flow. Despite this, its valuation has surged in 2025, fueled by regulatory tailwinds, U.S. policy support for nuclear and SMR technologies, and investor optimism around AI-driven energy demand.

Source: https://www.nrc.gov/reading-rm/doc-collections/news/2022/22-002.pdf

Source: Fxleaders

Recent Catalysts Strengthening the Story

Regulatory Progress

- In July 2025, Oklo successfully completed a readiness assessment with the NRC for its Aurora reactor license application. While the NRC previously rejected its first application in 2022 for missing details, this milestone signals improved preparation.

- The NRC has also accepted Oklo’s licensed operator model report for review

Federal Policy Tailwinds

- The U.S. ADVANCE Act (2024) is reshaping nuclear regulation, lowering fees by 55% (effective October 2025) and expediting reactor licensing.

- Nuclear is now positioned as a cornerstone of energy security and AI-driven infrastructure. (A long we look to add to our portfolio is nuclear energy once we see further progress and industry clarity)

Contracts & Partnerships

- LOIs and early agreements with data center operators (e.g., Switch) and U.S. defense installations (notably an Air Force base in Alaska) provide credibility.

- Collaboration with Vertiv aims to integrate Aurora’s energy with advanced cooling for AI data centers.

DOE Pilot Program

- In August 2025, Oklo was selected for three projects under the DOE’s reactor pilot program, alongside its subsidiary Atomic Alchemy. This validates the design but is not yet revenue-generating.

Market Sentiment

- The AI and energy narrative has fueled investor enthusiasm. Analysts have issued price targets in the $65–90 range, but the stock trades far above those levels. Insider selling has been notable, suggesting caution among company insiders.

Catalyst Timeline

NRC license application review (2025–2026)

DOE pilot program milestones (2025–2027)

Binding PPAs with data centers (2026+)

First Aurora deployment target (2027–2028)

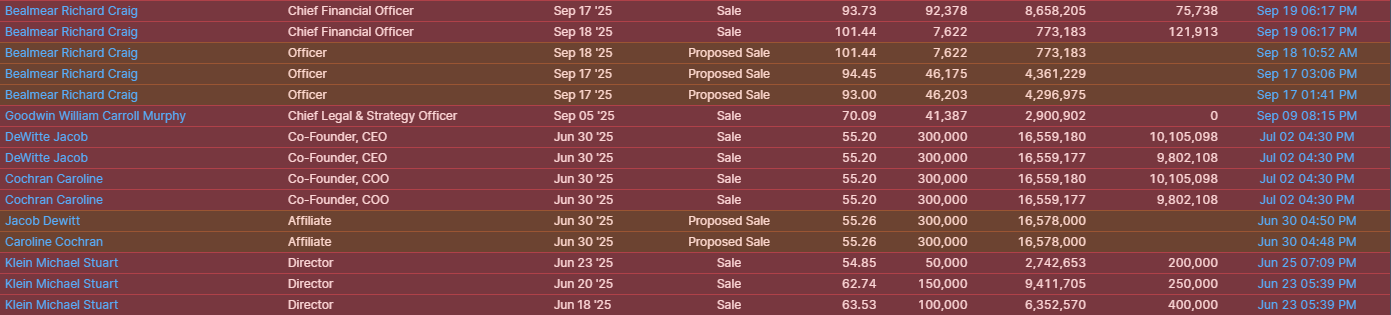

Insider Selling

One element investors should weigh carefully is insider behavior. Over the past three months, several Oklo executives and directors have been actively selling shares:

CFO Richard Craig Bealmear sold shares on Sept 17–18 at $93–101, realizing over $8.6 million, with further proposed sales filed in the same range.

Chief Legal & Strategy Officer William Goodwin sold shares on September 5, 2025, at $70.09, realizing nearly $2.9 million.

Co-Founders Jacob DeWitte (CEO) and Caroline Cochran (COO) each sold 300,000 shares on June 30, 2025, at $55.20, raising over $16.5 million apiece.

Director Michael Stuart Klein executed multiple sales between June 18 and June 23, 2025, at prices from $54.85 to $63.53, for proceeds above $6.3 million.

While these catalysts highlight momentum, insider behavior tells a more cautious story.

Source: Finviz Elite

Source: Finviz Elite

Fundamentally

Oklo has become one of the hottest stories in nuclear innovation, sitting right where clean energy meets the AI data center boom.

But the stock’s rise from under $10 last fall to over $135 today isn’t rooted in revenues or profits….because there aren’t any yet. Instead, the rally is built on expectations: regulatory breakthroughs, government support, and long-term partnerships with hyperscale data centers and defense. It’s an exciting vision, but investors need to remember that this is still a pre-revenue company with heavy quarterly losses and a long road ahead before Aurora reactors generate a single megawatt for paying customers.

When we run a valuation model, even with generous assumptions — Aurora reactors online by 2027–2028, successful NRC licensing, and PPAs converting into long-term cash flow — we arrive at fair value closer to $60–80 a share in a base case. A bull scenario, with faster approvals and smooth execution, could stretch into the $90–110 range, but that requires a near-perfect outcome. On the other side, if delays, cost overruns, or licensing issues resurface, fair value could quickly compress into the $30–$50 range. Against a current price near $135, the risk-reward balance skews heavily toward caution.

That doesn’t make Oklo un-investable, far from it. The company’s partnerships, DOE pilot program selection, and alignment with national energy security goals make it one of the most compelling long-term stories in the sector. But in the near term, we expect the stock to consolidate into the $70–90 range before it can establish a durable bottom and resume higher. For now, it’s a stock where patience pays, and timing matters as much as the technology.

Key Data at a Glance

Current Price: $135.23

52-Week Range: $6.42 – $110.82

Market Cap: Around $20B

Q2 2025 Net Loss: $24.7M

Revenue: None to date (pre-commercial)

P/E: Not meaningful / negative (due to losses)

Source: Finviz Elite

The chart below for OKLO shows one of the most dramatic rallies in the clean energy space this year…. After spending much of the past twelve months consolidating between $25 and $80, shares have broken out aggressively, surging more than 83% in a single session to $135.23.

The volume profile on the right shows the heaviest trading interest clustered between $35 and $80, which is now well below current levels. These zones represent potential areas of support if the stock retraces. The key moving averages also support those levels, and potential short targets. Technically, the breakout has left the stock extended, with parabolic candles suggesting short-term froth. For long-term investors, the chart highlights how far current pricing has run ahead of its historical base, making a consolidation or retest toward the $70–90 zone both likely and healthy before any sustainable next leg higher. That is a significant move down when gravity kicks in.

Source: Seeking Alpha Premium

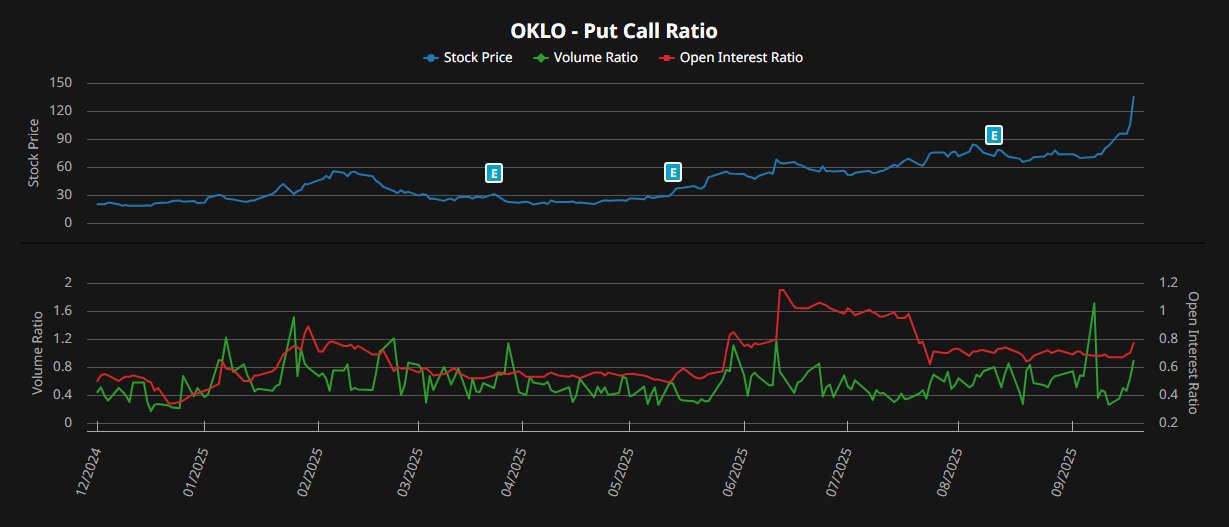

Options Market Signals

As always, we have to look and options tape is sending a clear message.

Put/Call Volume Ratio: 1.17 — more puts than calls trading of recent, showing short-term hedging and or bearish bets theme building into the rally.

Put/Call Open Interest Ratio: 0.70 — longer-term positioning still favors calls, so the bigger picture isn’t outright bearish.

Volumes: Around 197k puts vs. 168k calls traded, a spike in downside protection as the stock hit highs.

In plain terms: traders seem to be leaning defensively into strength. The short-term options flow matches the chart — frothy and over extended— while open interest shows there’s still belief in the story longer-term. This supports the tactical short view in my opinion, fading near-term excess while keeping the long-term vision intact.

Source: Barchart

Tactical View: A Short Before the Long?

With Oklo closing at $135.23 after an 83% single-session spike, the setup looks stretched well beyond both fundamentals and technical support. The stock has ripped far above its heaviest trading zones, leaving $70–90 as the most logical area where real buying support sits. Add to that the steady insider selling from co-founders and the CFO, and it’s hard to ignore that management sees this price level as an opportunity to take some chips off the table.

From a trading angle, that sets up a short-term short case. The stock is:

Overextended technically, with parabolic candles and RSI signaling exhaustion.

Detached from fundamentals, trading at ~10x our base-case fair value despite being pre-revenue.

Likely to consolidate, with strong support between $71–79 and a deeper base closer to $40.

For traders, fading strength in the $130–140 range could make sense. If shares break decisively above $150 with strong volume, that would weaken the short thesis and force a considerable reassessment. Near term, we see downside risk into the $90s, with a stretch target of $70–80. To be clear, this isn’t a knock on Oklo’s long-term potential at all… the company has real promise at the crossroads of nuclear energy and AI demand, a sector we watch closely to add some eventual-weighting in. It’s simply about timing: letting the froth bleed off and waiting for the next bottoming process offers a cleaner long entry.

In short, we’re neutral overall but tactically bearish in the near term. A sharper pullback or consolidation feels not just likely but necessary before Oklo can mount a sustainable rally. If the stock keeps running, we’ll reassess, but for patient investors the smarter trade may be to short the excess now, then flip long once key support levels confirm.

Conclusion

Oklo has carved out a unique position at the intersection of advanced nuclear and AI-driven energy demand, two of the strongest long-term themes. Partnerships with DOE, defense, and private sector players add credibility, but the company is still pre-revenue, burning cash, and waiting on critical licensing progress. The stock has the hype and with it, volatility.

Insider sales underscore the risk of near-term overvaluation. While we’re neutral with no position, we expect consolidation toward the $70–90 zone before a durable bottom forms. From there, Oklo could be set up for its next leg higher once tangible project milestones are achieved.

Thanks for reading.

Not financial advice, this material is for independent research purposes only.