Micron Technologies - November 2025 Report

2025-11-21

Preface

Micron enters a critical phase of its cycle, where sentiment and narrative begin to hand the baton back to fundamentals. The stock has shown notable resilience amid a broader cooling across semis, and while recent pullbacks have been shallow by historical standards, a more complete normalization cannot be ruled out. A retest of the $150–$155 region; anchored by the 100-DMA and a major volume support zone would represent a constructive reset rather than a deterioration of the underlying thesis. Then we hold 200 and 250? Let’s not get to ahead of ourselves just yet.

We have previously highlighted Micron as one of the most compelling under-recognized beneficiaries of AI infrastructure demand, and we exited our long exposure near $190 as the risk/reward began to skew less favorably. At the time of writing, we have no active position.

The December 17 Q1 FY2026 report will be a pivotal catalyst and vol-event. HBM traction, data center demand, and structural mix improvement support a strong long-term case. However, the near term remains sensitive to macro volatility, semiconductor supply/demand dynamics, and an increasingly complex geopolitical backdrop. The upcoming print will help determine whether Micron reasserts its leadership into 2026 or whether the market is recalibrating expectations after an exceptional run.

Source: Micron Technologies

Investment Thesis

Micron provides direct exposure to the AI compute stack through HBM, data center DRAM, and NAND. The company has rapidly gained traction in HBM, expanded gross margins, and built visibility into 2026 through contracted capacity.

Structural bull case

AI workloads drive serious memory demand.

HBM3E and HBM4 adoption accelerate content per accelerator.

Micron’s capacity is sold out for 2026, supporting pricing power.

Margin expansion is tracking ahead of pre-AI cycles.

Balance sheet is healthy, enabling continued capex and share capture.

Strong partner/client network (very)

Structural bear case

Memory cycles remain intact despite AI, with typical oversupply risk.

HBM capacity additions across the industry may pressure pricing post-2026.

AI demand assumptions may flatten if infrastructure build slows.

Competition from SK Hynix and Samsung remains intense.

Valuation depends heavily on FY2026 earnings holding up.

The long-term setup is constructive, but not without risks. The short-term picture depends on whether the correction stabilizes or deepens toward major support.

End Markets That Matter

Source: MU 2025 Investor Deck

Data Center (54% of Q4 revenue)

Cloud and core data center revenue reached $6.1B in FQ4, representing the primary AI-driven growth engine. HBM, DRAM, and NAND power AI training and inference clusters, making this the segment with the strongest margin expansion.

Client PC (33%)

Mobile and client contributed $3.8B. Not a high-growth market, but steady. economics.

Automotive (13%)

Auto and embedded revenue reached $1.4B. Vehicles are becoming rolling compute platforms, increasing memory content per car. Growth is slower, but durable and cycle-resistant?

Mobile (within the same 33%)

Smartphones continue to increase memory content due to richer apps, 5G, and emerging on-device AI.

Key Data Snapshot

Financial Metrics

Stock Price: $207.37

Market Cap: $232.77B

Revenue (TTM): $37.38B

Gross Margin (TTM): 39.79%

Gross Margin FY26 guidance: Around 51.5%

Forward P/E: Aproximate 12x (based on FY26 earnings expectations)

Cash & Investments: Around $11.94B

Debt: Around $14B

Debt-to-Equity: Around 0.26

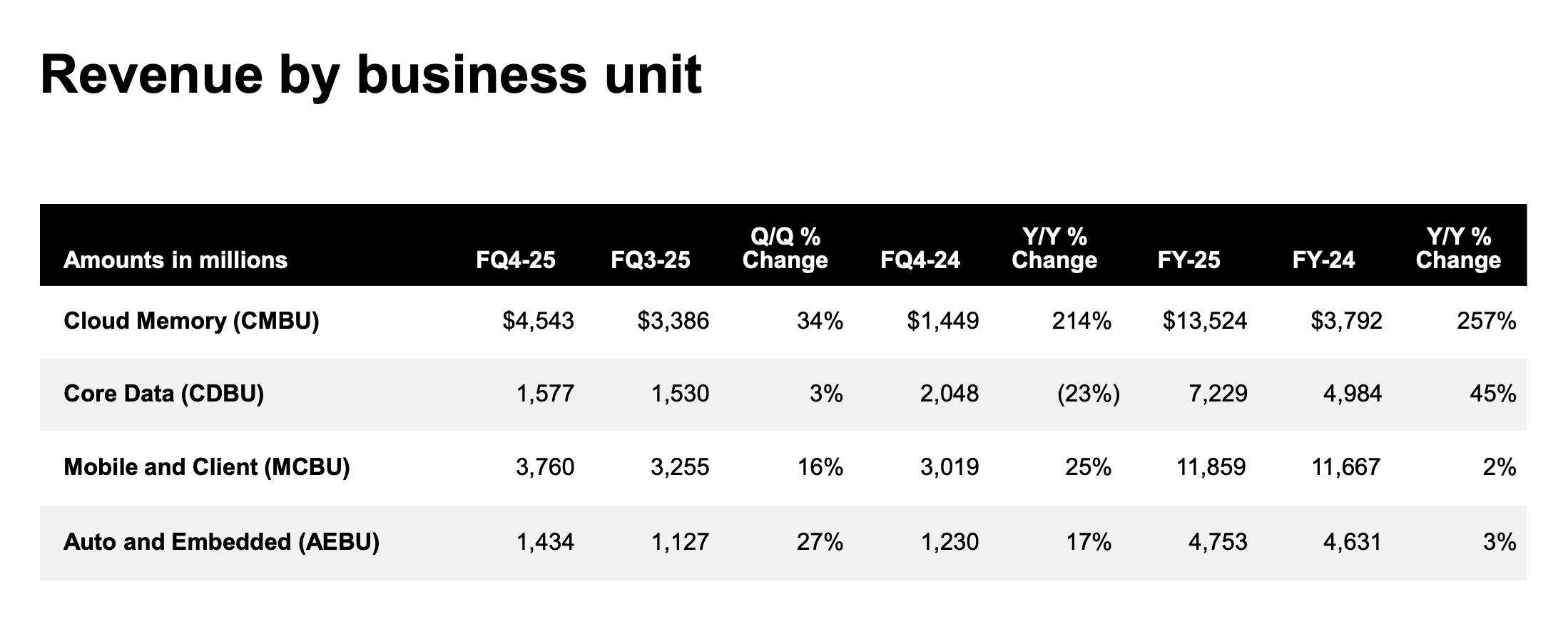

Segment Performance (FQ4 2025)

Cloud Memory: $4.54B revenue, 59% GM, 48% OM

Core Data: $1.58B revenue, 41% GM, 25% OM

Mobile & Client: $3.76B revenue, 36% GM, 29% OM

Auto & Embedded: $1.43B revenue, 31% GM, 20% OM

HBM and data center DRAM are now the clear growth catalysts driving both revenue and strong margin improvement.

Competitive & Market Positioning

Micron remains one of the three global leaders in DRAM, holding approximately 25% revenue share as of Q1 2025 (according to Counterpoint Research). SK Hynix leads with 36%, followed closely by Samsung at 34%, with the remaining 5% split across smaller regional suppliers. SK and Samsung remain credible peers no doubt, with meaningful exposure to the same cycle, but their U.S. OTC listings make them less accessible for many investors.

This concentration matters. DRAM is still the largest contributor to Micron’s revenue and the foundation of its cost and margin structure. A tight three-player market historically supports disciplined supply growth, coordinated capex behavior and more stable pricing; critical dynamics as the industry shifts toward AI-oriented memory such as HBM and high-performance DRAM.

Micron’s 25% market share reflects both competitive execution and the company’s position as the only US-based scaled DRAM producer. While SK Hynix currently dominates HBM, Micron’s progress in advanced DRAM nodes and its diversification across data center, mobile, automotive and PC markets keeps share stable and positions the company to participate directly in AI-driven memory demand cycles.

HBM Market Share (Q2 2025): Around 21%

SK Hynix: Around 62%

Samsung: Around 15%

Micron’s HBM capacity: * fully committed for 2026 *

HBM revenue run rate: Around $8B annualized

Peers across the AI compute stack: NVIDIA, AMD, Intel

Micron has moved from a trailing participant to a competitive player in high-value memory. The strategic question is whether this share can expand as HBM4 ramps, or whether industry-wide buildout caps pricing power.

A Controlled Correction?

Source: Seeking Alpha Prememium - 24K Research

Micron has shifted from a strong trend into a meaningful cooling phase. Price lost the short-term moving averages, momentum rolled over, and volume favored sellers into the pullback.

Key zones

Support: 193–187 (light), then the larger key 175–150 volume shelf (a well targeted potential accumulation point to watch for).

Resistance: 200–220 (the “decision zone”) … we could very well see this level broken out of as a strong Q1 2026 earnings guidance is delivered on.

A decisive move above 220 would indicate buyers regaining control and the correction resolving. A break lower opens room toward deeper support clusters where longer-term capital typically steps in.

The structure favors monitoring, not predicting, the next leg.

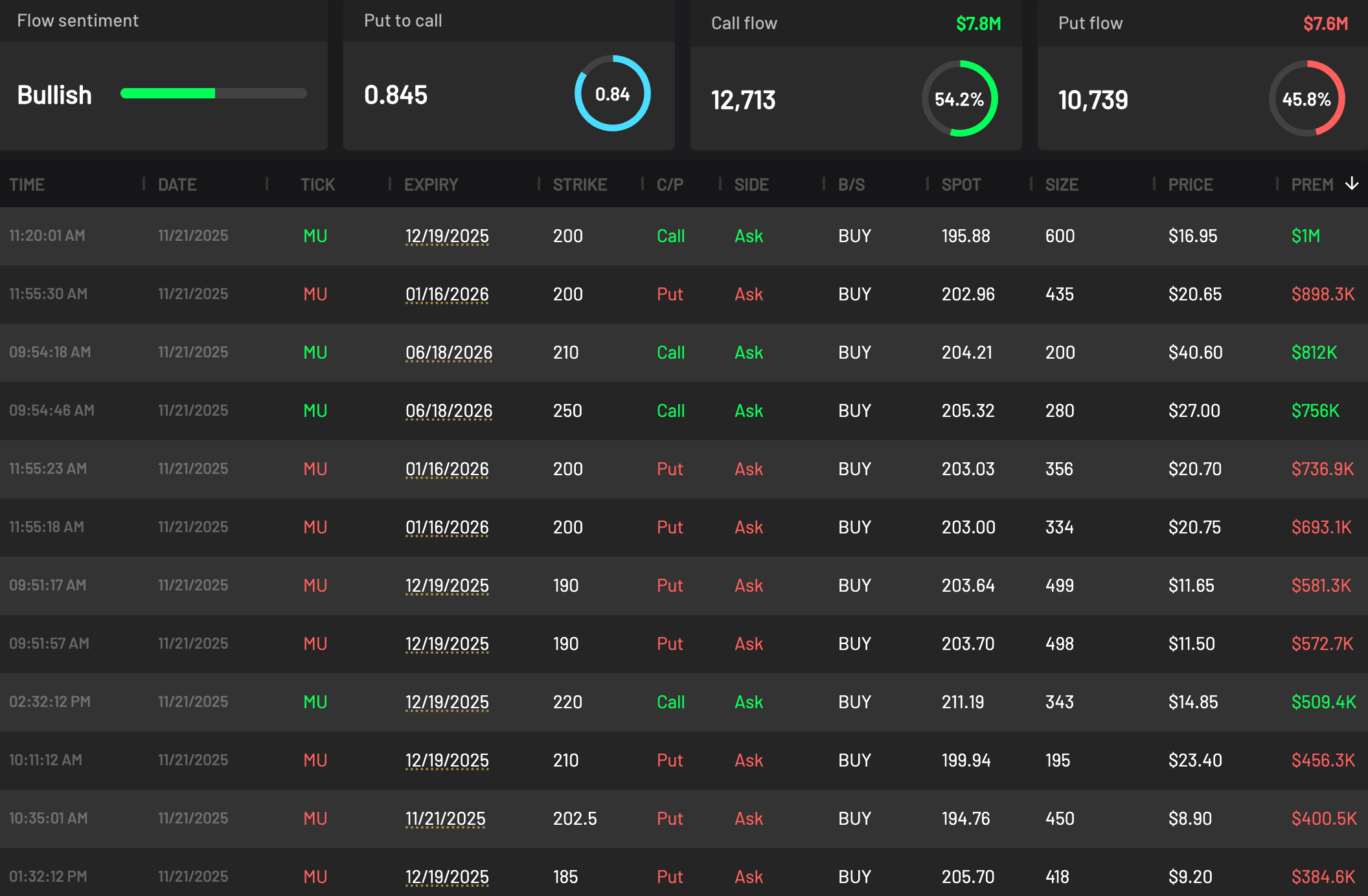

Options Flow

Source: Cheddar Flow Pro

Options flow shows bullish long-dated positioning paired with meaningful near-term hedging or bearish positioning. June calls saw strong interest, while December–January puts at 185–210 were actively accumulated. This signals confidence in long-term fundamentals but caution over short-term volatility.

Peer Positioning

Source: Seeking Alpha Premium MU Comp

YTD: Micron (+102%) has dramatically outperformed top-tier competitors.

AMD (+48%), Intel (+41%), Qualcomm (+5%), ARM (-1%), and Texas Instruments (-20%). This makes Micron the most aggressively repriced memory beneficiary of AI and also one of the most exposed to corrective pressure.

Q1 2026 Expectations and Roadmap

Key Q1 2026 Expectations

Revenue: Guided to $12.2B – $12.8B, tracking a record quarter.

EPS: Projected $3.75 ± $0.15 on stronger HBM mix.

Gross Margin: Expected at 51.5% ± 100 bps, implying sustained pricing strength.

HBM Supply: 2026 HBM3E capacity fully committed; HBM4 discussions underway.

DRAM Market: Industry supply tight, supporting elevated pricing and mix.

Summary

Micron’s December Q1 FY2026 report is shaping up as a defining moment for the AI memory cycle. Guidance is well above Street expectations and reflects a company benefiting directly from HBM demand, tight DRAM supply, and accelerating data center spending. The upcoming quarter will confirm whether Micron’s margin step-up is durable or simply the peak of a tight supply window.

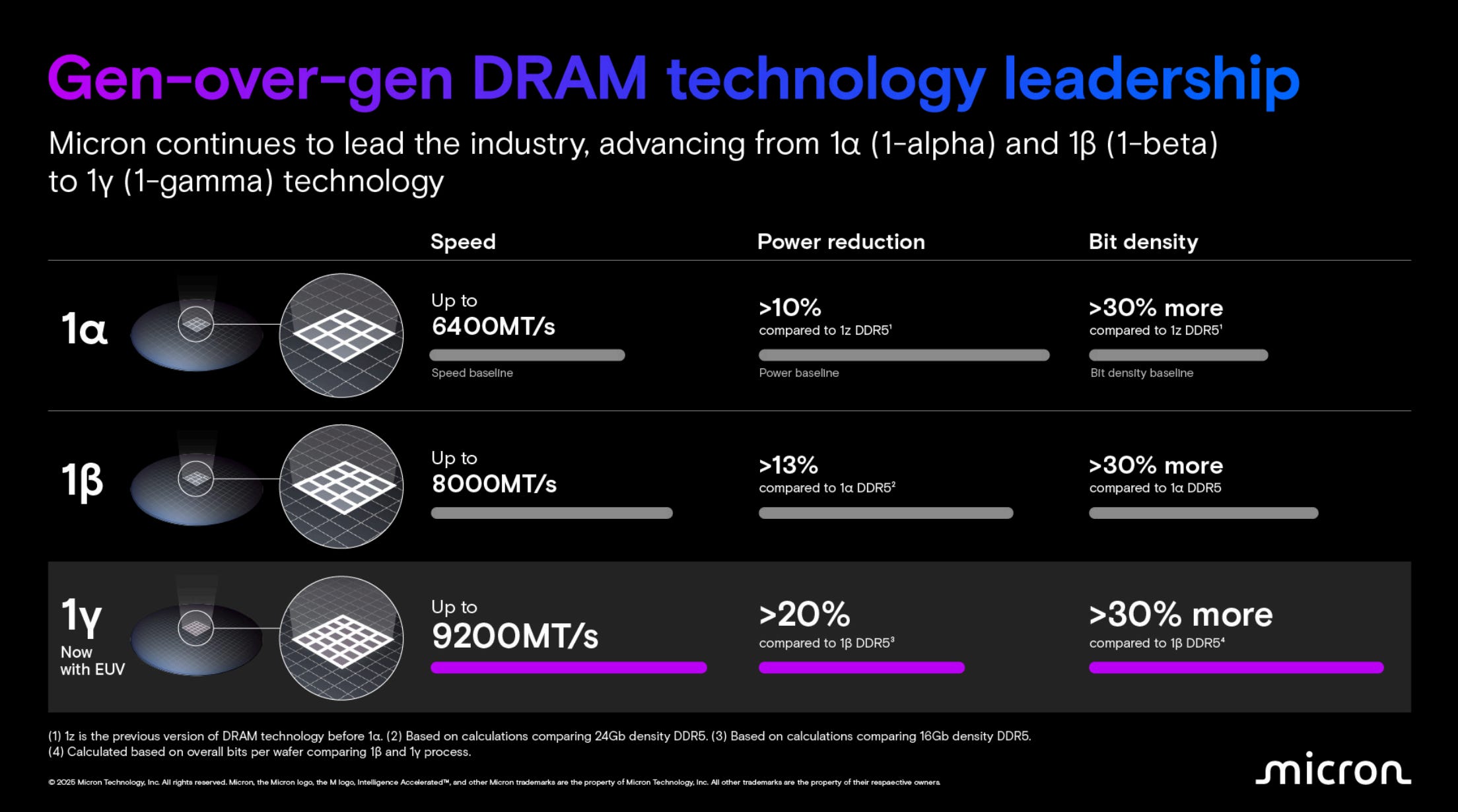

On the technology front, Micron’s roadmap remains the critical driver beyond the quarter. The ramp of 1-gamma DRAM will be central to cost reductions and competitive positioning. G9 NAND supports higher-density storage for AI workloads and enterprise SSD expansion.

Source: Micron Technologies Infographics

And the transition into HBM4 will determine whether Micron can meaningfully close the gap with SK Hynix and avoid margin erosion as capacity expands in 2026 and 2027.

Conclusion

Micron enters 2026 with a powerful long-term backdrop: HBM traction is real, AI infrastructure demand remains firm, and the margin profile is finally reflecting the immense value of high-performance memory. The company has visibility that few peers can match, US based; and if the AI cycle continues to accelerate, Micron is positioned to participate directly.

But the near-term setup is more balanced. Valuation depends on Q1-2026 earnings materializing, competitive supply from Hynix and Samsung is rising, and memory has not escaped its cyclicality, yet. Add geopolitical pressure, export controls, and the possibility of an AI capex cooldown, and the range of outcomes widens quickly. It is also impossible to ignore how far the stock has run. Even great stories need resets.

We remain hopeful the AI cycle takes full flight into 2026 and keeps the high-value memory theme intact. At the same time, we are fully prepared for the downside scenarios that come with this phase of the cycle: oversupply risk, macro cooling, and sentiment giving back excess, and remain unbiased. The next real signal will come from how Micron behaves around its major support zones and what management communicates in December. Until those confirm, a neutral, probability-driven stance is more than rational.

Not Financial Advice: This report reflects research, data interpretation and market context only. It is not a recommendation to buy or sell any security. Always evaluate your own risk tolerance and financial objectives before making investment decisions.