Marvell Technology: Assessing the Recovery Case

2025-08-28

Marvell just delivered pretty good Q2 numbers and closing-the $2.5B auto Ethernet divestiture, clearing the way to focus almost entirely on AI and data center growth. Unfortunately, a lot more than just some good numbers were needed to provide the W.

The story here is simple: massive opportunity ahead in custom silicon and optics, but timing and execution remain the swing factors. With shares now back near the 200W average $62-$64, -18% post earnings call, risk/reward looks more attractive than earlier this year — but it’s not a straight line up, it’s about finding a base. Things have been quiet and investors look for execution, this sets the stage.

Source: GettyImage

Big Growth, Balanced by Caution

Revenue came in at $2.06B, up 58% year over year and 6% sequentially

$0.67 non-GAAP EPS and a 35% operating margin.

Data center drove the show, accounting for 74% of revenue and growing 69% YoY.

Operating cash flow jumped to $462M

The company repurchased $200M of stock, leaving $2B authorized.

The good: AI demand is real, optics are delivering double-digit growth, and networking/carrier revenue rebounded 43% YoY. CEO Matt Murphy underscored that growth is being fueled by custom silicon, electro-optics, and a faster recovery in networking and carrier markets.

The caution: Q3 guidance came in at $2.06B (+36% YoY), slightly under Street estimates, with management noting “lumpiness” in custom shipments. The softer outlook triggered a sharp selloff — shares fell to $68 after hours and then slid another 5% to close near $62, down 18% in 24 hours and breaking below the 200-week average ($64).

Valuation: At current levels, Marvell trades at ~25–26x forward earnings — not cheap, but reasonable for semis if execution stays on track and growth stabilizes.

Source: Seeking Alpha Premium

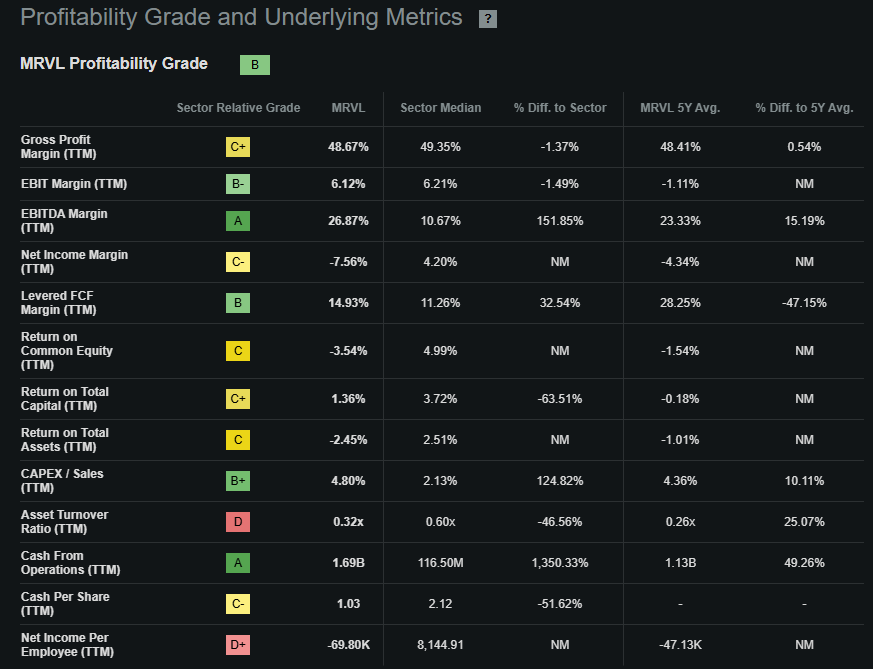

Marvell Profitability Snapshot

Marvell is generating strong cash flow…I did not say net income, and we wouldn’t be here if the price was not trying to find a new bottom.

27% EBITDA margin

14.9% free cash flow margin (TTM)

CapEx at 4.8% of sales is focused on AI and datacenter expansion.

GAAP net income margin remains negative (-7.6%), with ROE (-3.5%)

ROA (-2.5%) still under pressure from heavy R&D and buildout costs.

Source: Seeking Alpha Premium

Strategy Reset: All-In on AI

The auto Ethernet sale was more than a divestiture — it’s a pivot. That $2.5B deal gives Marvell more flexibility and narrows focus. Management sees 18 active sockets across hyperscalers and enterprise AI players, and a $94B data center TAM by 2028, up 26% from prior estimates. (Per Markbeat)

At its June AI day, Marvell highlighted 50+ custom design programs, many with multibillion-dollar lifetime potential. In short, they’re chasing bigger, stickier projects — but the timing of ramps will dictate the revenue line.

The story is straightforward…

The upside is real — custom silicon + optics are a massive opportunity.

The swing factor is timing and execution.

With shares back in the $62–$64 range, risk/reward looks improved compared to what it did earlier this year. Not a straight line up, more about the consideration based on how the stock consolidates over the next few.

Risks That Keep Volatility High & Analysts Uncertain

The main risk is still geopolitical, but when isn’t it…for Marvell, it is also timing. Even with strong design engagement, if projects take too long to hit production and investors don’t see execution, growth looks choppy. Management’s conservative guidance adds to that, especially with a market trained on “AI beats every quarter.” And with around 43% of revenue tied to China, and less than 20% in North America, trade policy remains a constant wildcard.

Source: Finviz Elite

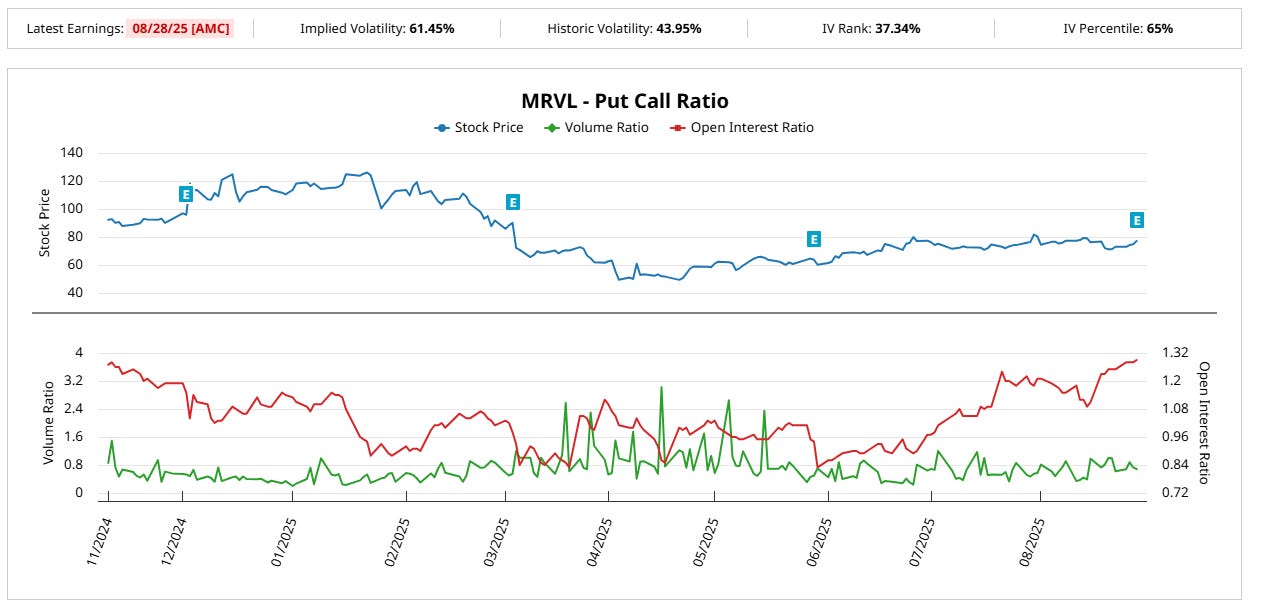

The put-call ratio on MRVL has been grinding higher through summer, with open interest now leaning more defensive — what looks like a sign traders are hedging or bracing for more chop even as the stock tries to base in the high-60s to mid-70s.

Source: Barchart

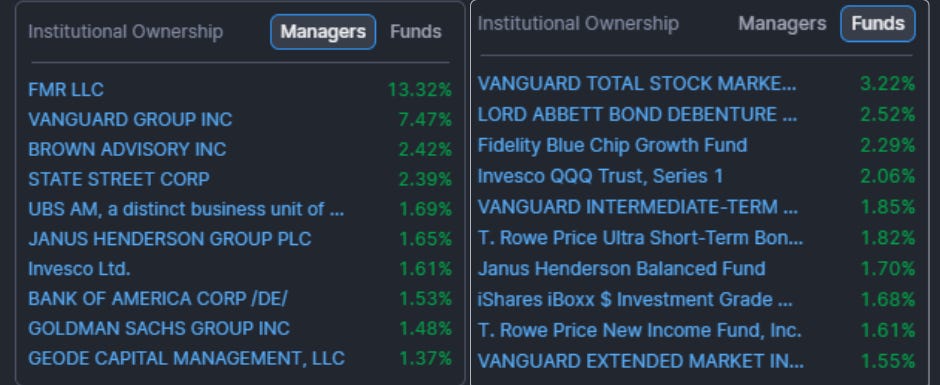

Institutional Ownership

Institutional ownership is balanced between passive giants and active growth funds. That provides stability but also means Marvell’s stock is highly correlated with ETF flows and sentiment toward growth/AI themes.

Source: Finviz Elite

High Priority Customers (Direct & Indirect)

Distributors: Wintech Microelectronics (China) handled ~34% of FY2025 revenue; Avnet and Arrow remain key global channels.

Hyperscalers/Cloud: Amazon (AWS), Microsoft (Azure), Google, and Meta are all tied to Marvell’s custom silicon and optics programs.

Networking/Telecom: Cisco (switch silicon), Nokia and Ciena (optical transport).

Storage/Enterprise: Western Digital, Seagate (storage controllers), plus Dell and HPE in servers and networking.

Upside Drivers

Conversion of custom AI chips from design wins into volume production

Sustained double-digit growth in optics

Margins lifting back above 60%

$2B+ buyback authorization providing additional support

From $63.00 at the moment (Updated 7:59pm PST), there’s room back to $100 (~30–35% upside) if execution clicks. On the downside, a slip into the $60-$61 is possible without cleaner revenue visibility. Goldman stayed neutral on $75 price target as of June 2025, which would be an ideal level to see a base form.

Conclusion

Marvell has clearly pivoted — exiting auto to go all-in on AI and data center. The demand backdrop and pipeline are there, but so are the challenges of hyperscale lumpiness and execution risk. What matters now is whether sequential growth holds and design wins actually scale into revenue. If that plays out, Marvell could participate in the asymmetric side of a broader V-shaped recovery, much like some of its peers. For investors, the story isn’t about chasing quick AI trades, but about watching how this transition unfolds, capitalizing on moves, backing winners and leaning in with patience as the evidence builds.

Thanks for reading!

Never Financial Advice. For research and informational purposes only.

Sources

https://app.quotemedia.com/data/downloadFiling?webmasterId=101533&ref=319002937&type=HTML&symbol=MRVL&cdn=d95b67590f0ebf75e481e13ae0fd7e60&companyName=Marvell+Technology+Inc.&formType=10-K&dateFiled=2025-03-12

https://www.marketbeat.com/earnings/reports/2025-8-28-marvell-technology-group-ltd-stock/?utm_source=chatgpt.com