Exploring Gilead Sciences (GILD)

12-7-2025

Preface

The “Wetware” Side of the Revolution?

In a market currently intoxicated by Large Language Models and silicon capacity, it is easy to forget that the original “source code” is DNA. While the world chases the infrastructure of compute; ourself included, we are also quietly exploring and when it makes sense, accumulating, the infrastructure of life.

Gilead has spent five years in the penalty box, dismissed as a relic of a bygone era. We believe this exile is over. They have successfully transitioned from a “hit-driven” chemical manufacturer to a “platform-driven” biological utility.

To confirm we do not have an active position currently.

Exploring Life Infrastructure

We are looking at Gilead Sciences not as a generic drugmaker but as a mispriced utility. For the past five years the market has viewed this company as a value trap with shrinking revenues. This view is now obsolete. We are entering a transition period where Gilead pivots from selling daily pills to managing a global delivery system for long acting HIV prevention. We are exploring the manufacturing capacity, the distribution channels, and the intellectual property that will tax the healthcare system for the next decade. The transition from a competitive commodity market to a recurring medical annuity is the core of this theme.

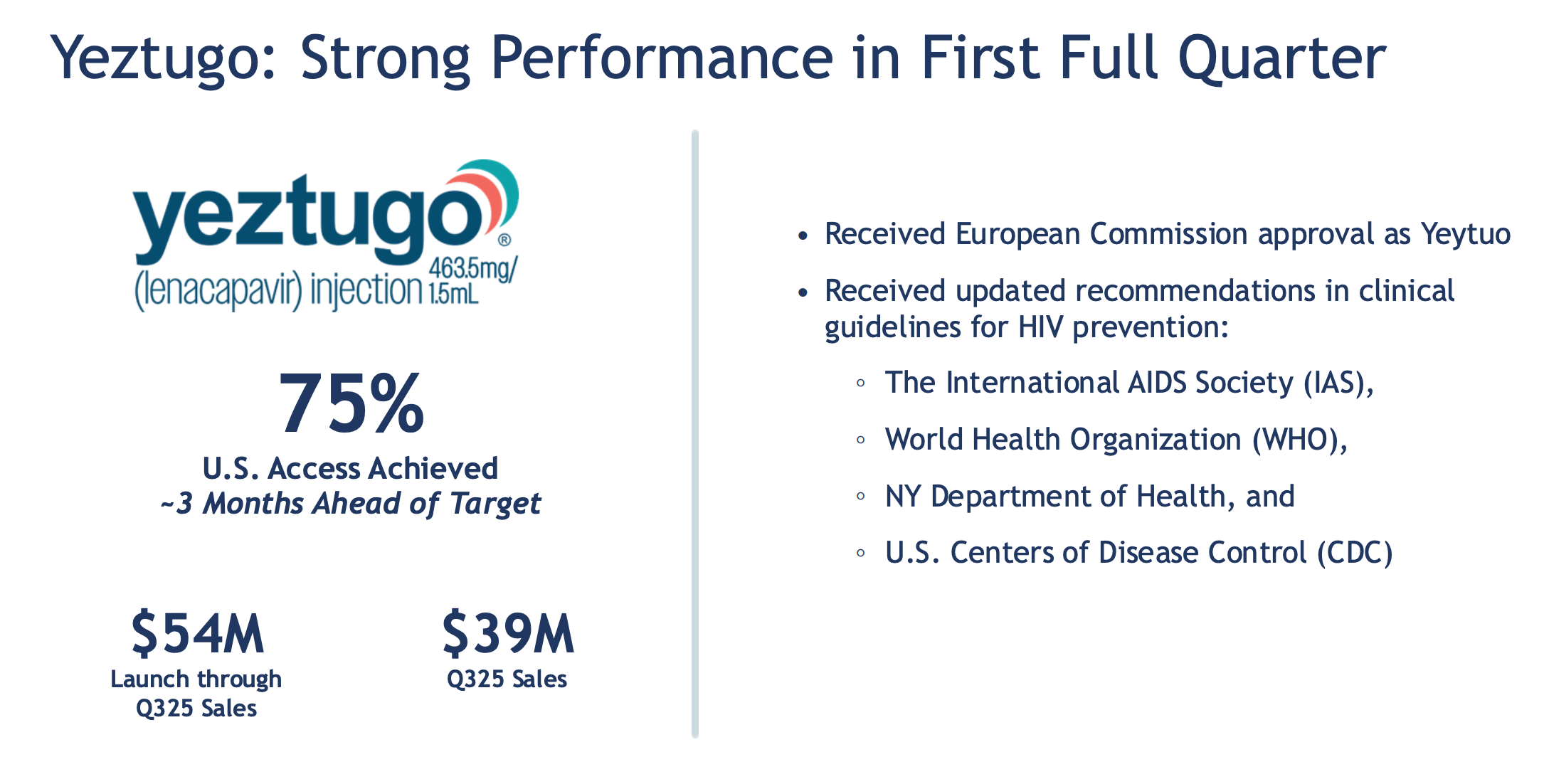

The Crown Jewel, The Yeztugo System.

Source: Gilead 3Q Presentation

The driver of this repricing is Lenacapavir (branded as Yeztugo).

This is not just another drug. It is a structural advancement in how HIV prevention is delivered.

Source: yeztugohcp

The clinical results are unprecedented. In the PURPOSE 1 and PURPOSE 2 trials Yeztugo demonstrated 99.9% to 100% efficacy in preventing HIV acquisition. This effectively renders the drug a functional vaccine for the duration of its activity.

By moving patients from a daily oral pill to a subcutaneous injection every six months Gilead fundamentally changes the business model. A daily pill relies on patient memory and willpower which leads to variable adherence and retention. A twice yearly injection administered by a healthcare professional guarantees compliance. This mathematically increases the lifetime value of every patient and creates a high friction cost for switching to a competitor.

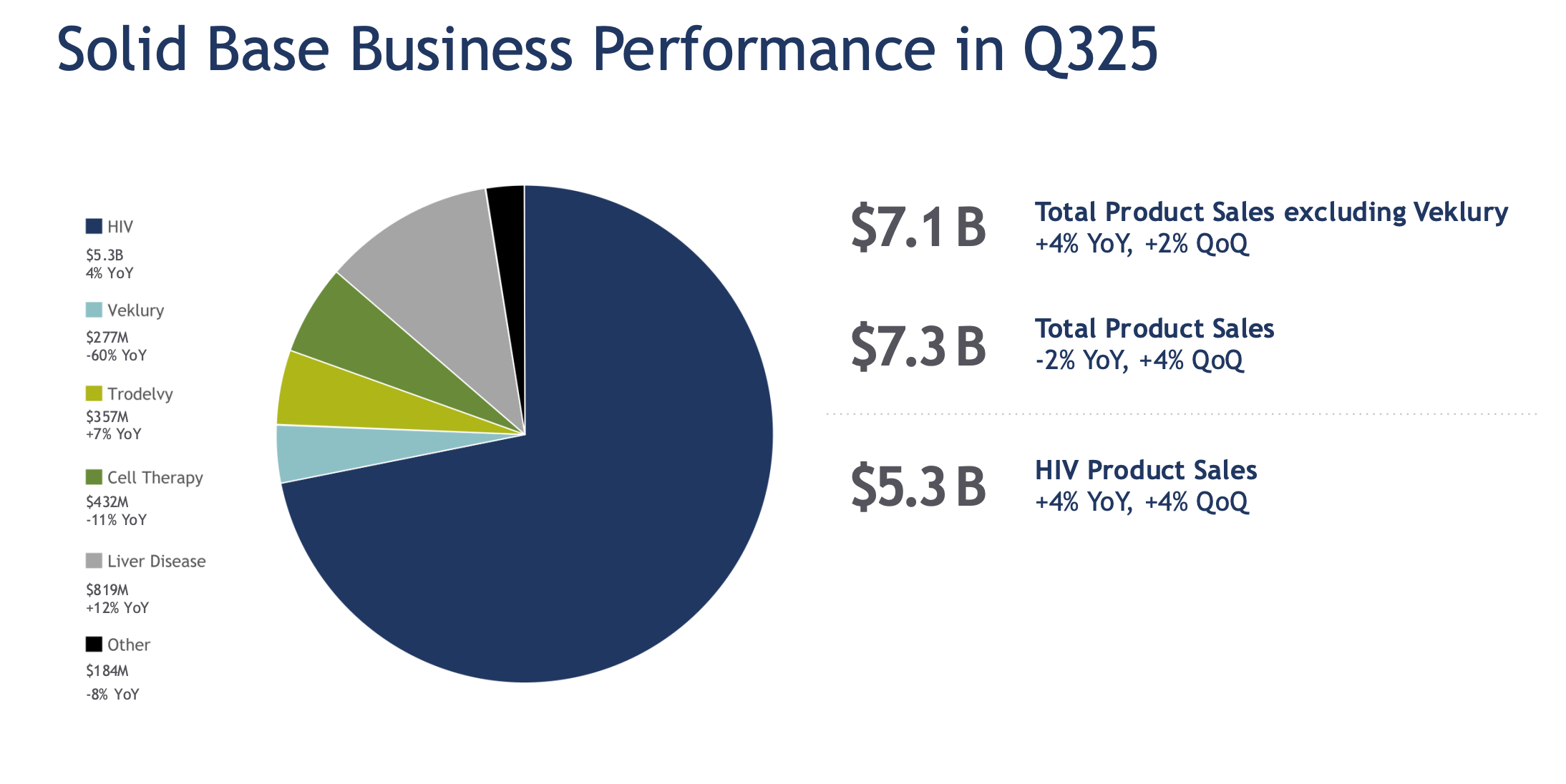

Established Income Streams

Source: Gilead 3Q Presentation

While Yeztugo represents high growth velocity, the existing infrastructure is supported by sizeable, strong cash flow generators that provide stability.

Biktarvy (The Anchor) Biktarvy remains the absolute standard of care in HIV treatment.

Dominance: It generated $3.7 billion in revenue in Q3 2025 alone, up 6% year over year.

Market Share: The drug commands approximately 52% of the treatment market in the United States.

Durability: Patent exclusivity has been extended into 2036, securing this cash flow stream for another decade.

Diversified Growth Engines Beyond HIV, the infrastructure is reinforced by growing franchises in Oncology and Liver Disease.

Oncology: Trodelvy sales reached $357 million in Q3 2025 (up 7% year over year), despite market headwinds.

Liver Disease: The portfolio delivered $819 million in the quarter, with the new drug Livdelzi surging 35% sequentially.

Revenue Quality The quality of this revenue is exceptional due to the “sticky” nature of the products. The shift from daily pills (Biktarvy/Descovy) to long acting injectables (Yeztugo) transitions the revenue model from a consumer product dynamic to a predictable, service like utility model with high switching costs.

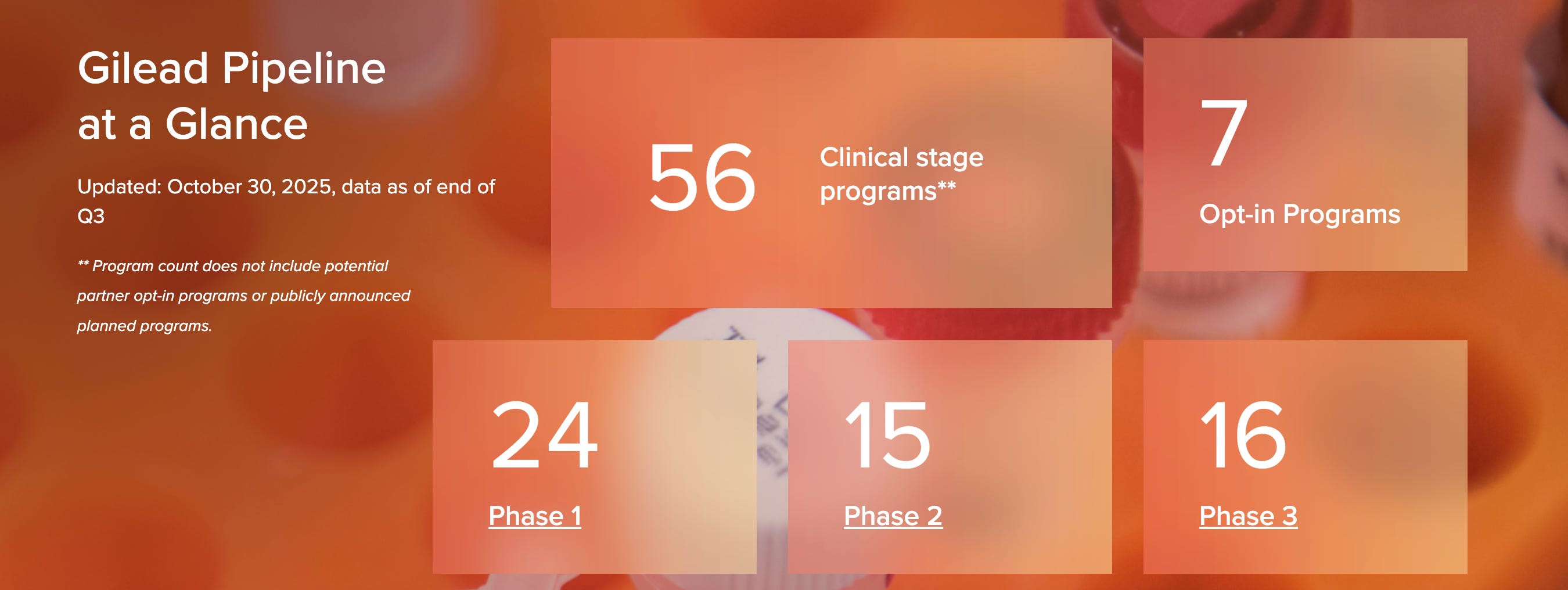

R&D Pipeline Architecture

Source: Gilead Sciences

The durability of Gilead’s infrastructure is supported by a diversified and balanced clinical funnel. As of Q3 2025, the company maintains 56 clinical stage programs, ensuring multiple shots on goal across varying therapeutic areas.

Funnel Composition The asset distribution shows a healthy “wedge” shape, prioritizing long term sustainability alongside immediate commercial opportunities.

Early Stage Breadth (Phase 1)

The 24 programs in Phase 1 represent a wide innovation funnel, essential for mitigating patent cliffs in the next decade.

Strategic Optionality

Beyond internal development, the 7 opt in programs provide external leverage, allowing the company to expand its reach without immediate capital allocation.

Late Stage Velocity

With 16 programs in Phase 3, the infrastructure is primed for near term regulatory catalysts and revenue replacement.

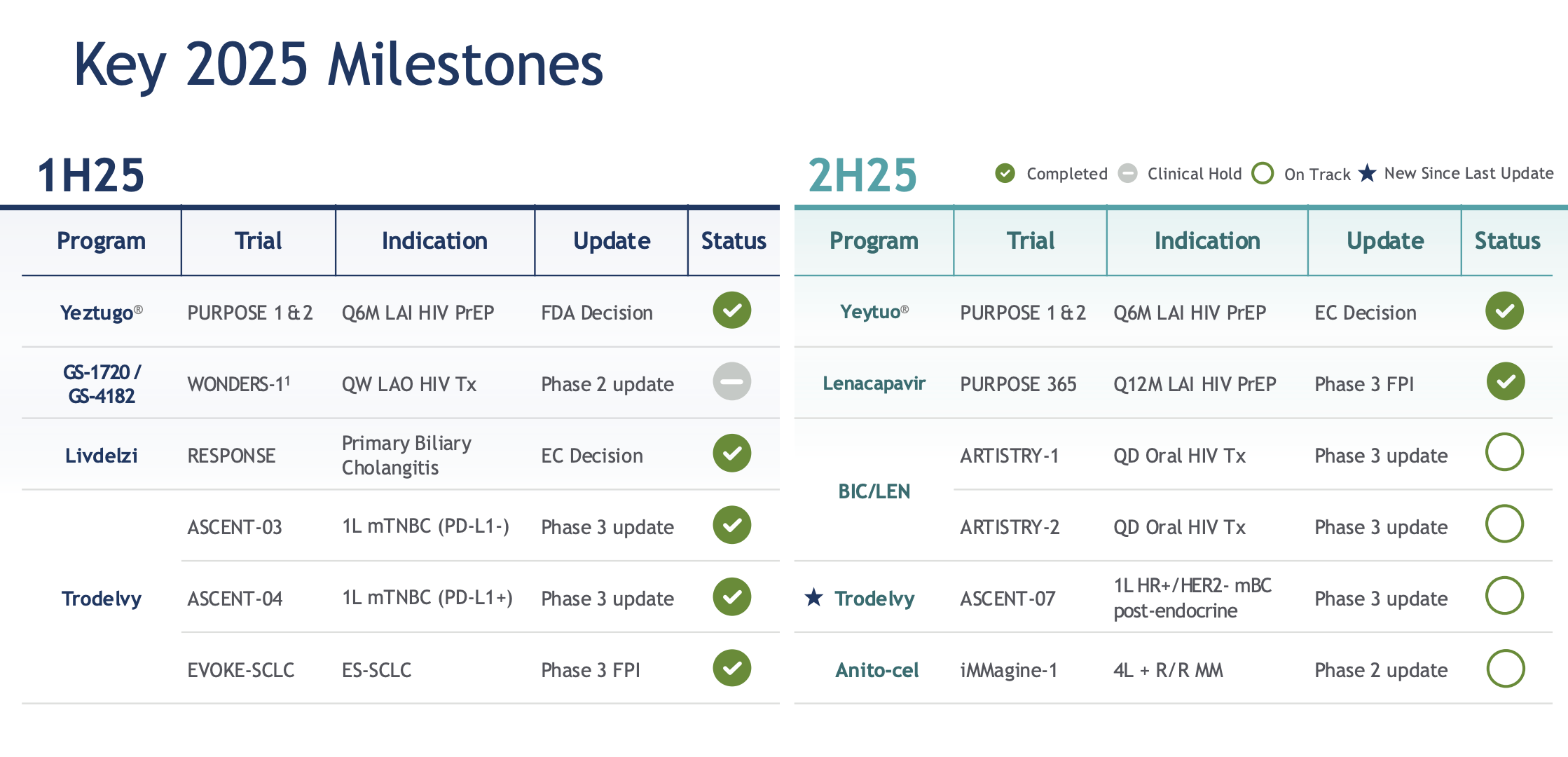

Key Milestones

Source: Gilead 3Q Presentation

The 2025 milestone scorecard validates a period of exceptional operational execution, characterized by the successful clearance of major regulatory hurdles—most notably the FDA and EC decisions for Yeztugo. With these binary events now resolved, the investment narrative shifts entirely from clinical probability to commercial reality, magnifying the Q1 2026 execution risk identified in our thesis. While the clinical hold on GS-1720 temporarily constrains oral diversification, the “On Track” status of the ASCENT-07 readout for 2H25 serves as the critical firewall to defend the oncology franchise against competitive erosion.

The Empire: What You Actually Own.

Source: KitePharma

When you buy GILD you are acquiring a fully integrated biopharmaceutical engine that powers four distinct high value innovation centers.

The Engine, Kite Pharma is the undisputed leader in Cell Therapy (CAR T). This division engineers patient specific T cells to combat blood cancers and represents the futurist wing of the company. CymaBay Therapeutics was acquired in 2024 to secure Seladelpar (Livdelzi). This is a best in class asset for liver disease that is already accretive to revenue. Immunomedics anchors the oncology strategy with Trodelvy which is the cornerstone drug for solid tumors.

The Force Multipliers

Strategic partnerships allow Gilead to de risk development while retaining commercial upside. They are working with Arcellx ACLX 0.00%↑ on next generation cell therapy for multiple myeloma and have entered a rare collaboration with Merck MRK 0.00%↑ to combine their assets into a once weekly oral treatment.

The Arcellx Connection (ACLX)

Our long-standing tracking of Arcellx was never about hype; it was about the superior physics of their “D-Domain” synthetic binder…which solves the structural instability of legacy CAR-T. The recent Phase 2 iMMagine-1 data presented at ASH confirms our thesis: this technology turns artisanal biology into scalable industrial design, delivering a “force multiplier” for Gilead that offers best-in-class potency without the toxicity profile of competitors.

Efficacy: Delivered a 96% Overall Response Rate with 74% Complete Response.

Safety: Zero cases of delayed neurotoxicity or Parkinsonian symptoms observed.

Execution: High manufacturing success rate; on track for 2026 commercial launch.

Financials, The Fortress (Q3 2025 Data)

The latest numbers confirm the infrastructure thesis. We see a balance sheet capable of absorbing macro shocks while fully funding the dividend.

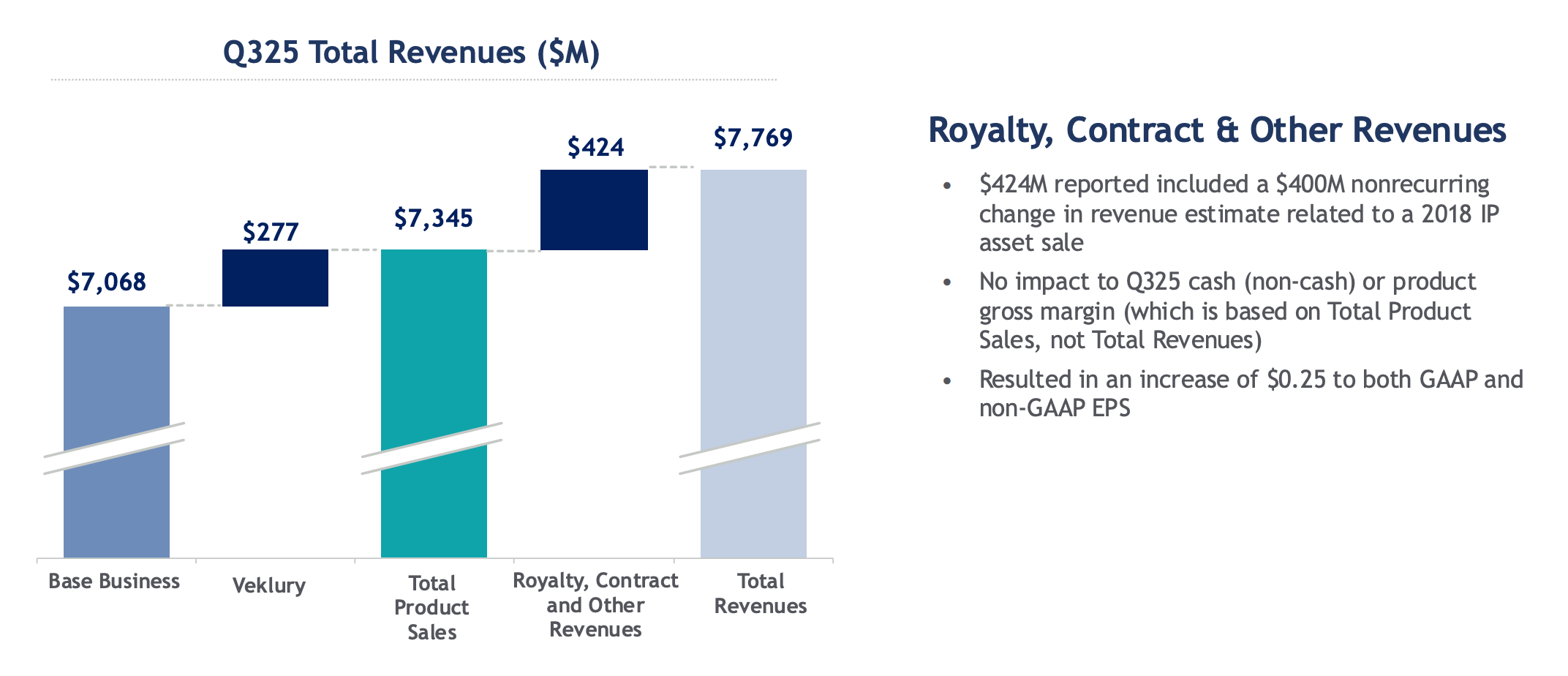

Revenue: $7.8 Billion. Beat expectations by ~$350M.

Operating Cash Flow: $4.1 Billion. This is the critical number. It represents massive utility grade cash generation.

Cash on Hand: $9.4 Billion. Includes cash equivalents and marketable securities.

Total Debt: ~$25.0 Billion. Leverage is present, with a moderately healthy Cash to Debt ratio of ~0.38.

EPS (Diluted): $2.43. Up significantly from $1.00 in Q3 2024 proving the earnings leverage is real.

P/E Ratio: ~12x to 14x. The stock trades at a utility multiple rather than a growth multiple offering a margin of safety.

Capital Allocation, The Safety Net

Sources: Gilead 3Q Presentation

While we hedge against potential Q1 volatility, Gilead is effectively paying us to wait. In Q3 alone, the company returned $1.4B to shareholders….paying out $1B in dividends and repurchasing $435M in stock at an average price of $113.25.

Critically, this payout is supported by the stability of the core franchise. The “Base Business” which grew +4% year-over-year to $7.1 billion, successfully overpowering a 60% collapse in COVID-related sales.

Investors should be careful not to misread the headline Total Revenue number of $7.77 billion, which was optically boosted by a $400 million non-recurring accounting adjustment related to a 2018 IP sale. This $400 million was a non-cash event. By stripping that out, we see the reality: a steady, cash-generative core business that funds the yield and protects the downside while the Yeztugo launch matures.

Risks…The Seasonality Trap?

While the long term thesis is robust we must identify the specific structural risks that could derail the stock in the short term.

The Q1 2026 Expectation Mismatch….The greatest near term risk is a collision between analyst expectations and historical reality. Wall Street is currently projecting a massive +13% earnings growth for Q1 2026. This creates a dangerous setup. The first quarter is historically Gilead’s weakest period due to US insurance deductible resets which often cause patients to delay expensive prescriptions. If the Yeztugo launch encounters any logistical friction and fails to overpower this seasonal drag the company will miss that aggressive target.

Oncology Execution… Gilead invested billions to pivot into Oncology but they face stiff competition from titans like AstraZeneca. If Trodelvy growth decelerates it drags on the Return on Invested Capital (ROIC) and weakens the diversification narrative.

Strategic Consideration: The Hedge

Given the Q1 seasonality risk outlined above we can structure the trade to improve our probability of success.

The Play If you are long the stock the historical weakness in Q1 suggests a tactical opportunity. One might consider selling Covered Calls against the position (perhaps the April 2026 strikes) to harvest premium. This acts as a mild hedge against a potential earnings miss in early 2026. Alternatively if the stock dips on a “seasonal miss” in Q1 or Q3, we view this as a high conviction accumulation zone rather than a thesis breaker.

Conclusion

Gilead is the adult in the room. While many other biotechs burn cash hoping for a miracle Gilead prints $4B a quarter from an established infrastructure while slowly rolling out a monopoly in HIV prevention.

We continue to analyze and consider a position, with an emphasis on Q1 2026 bringing a potential accumulation opportuntity.

Disclaimer - This is Not Financial Advice. The content provided by 24K Research, including all reports, newsletters, articles, and communications, is for informational and educational purposes only. It should not be construed as professional financial advice, investment recommendations, or a solicitation to buy or sell any securities, derivatives, or financial instruments.

Sources

https://investors.gilead.com/financials/sec-filings

https://investors.gilead.com/financials/quarterly-earnings

https://www.sec.gov/edgar/browse/?CIK=882095