DDOG - January 2026

2025-01-22

Founded in 2010 in New York City, Datadog has established itself as the premier unified observability platform for the cloud era. By integrating infrastructure monitoring, log management, and application performance monitoring (APM) into a single interface, the company breaks down critical silos between DevOps and Security teams. As the global software stack reaches a breaking point, Datadog is aggressively transitioning from a elite monitoring utility into the foundational observability layer for the nascent AI infrastructure era; with the revenue growth moving along already to back it.

In 2026, downtime is no longer just an IT headache, it is a catastrophic loss of revenue and reputation. As enterprises shift from basic cloud migration to complex, agentic AI ecosystems, the "visibility tax" has risen. Organizations cannot manage what they cannot see. Datadog (DDOG) has pretty much evolved from a simple infrastructure monitor into the essential "Single Pane of Glass" for the modern CTO, consolidating observability, security, and AI performance into one high-velocity platform.

Thesis

Source: Saleforce Dev Ops / DDOG

Datadog’s primary value proposition is the Flywheel of Complexity.

As enterprises transition from legacy servers to fragmented, multi-cloud architectures and agentic AI models, the “visibility tax” becomes almost unavoidable…. Datadog has positioned itself as the essential central nervous system, breaking down silos between DevOps and Security teams. By aggregating billions of real-time data points across infrastructure, logs, and traces, the platform transforms technical noise into actionable intelligence. A key feature driving this shift is Watchdog, an AI-driven anomaly detection engine that surfaces performance regressions and root causes automatically, often before a human responder is even alerted.

The second pillar of our thesis is the AI Sentinel Effect. Datadog is uniquely positioned as the “monitor of the monitors” for the generative AI boom. With marquee clients like OpenAI using the platform to track GPU utilization, token latency, and model performance, Datadog has captured the highest-value workloads in the modern economy. This creates a powerful competitive moat: while rivals focus on legacy log management, Datadog is becoming the infrastructure layer for the next decade of autonomous software. We view the stock as a core compounder that thrives on technical chaos and vendor consolidation.

Revenue Quality

Source: Finviz Elite DataDog

DDOG

Current Price $131.25 (+$7.78 / +6.3%)

Market Cap $46.03B

Revenue $3.21B

52-Week High $201

52-Week Low $81

Datadog’s financial profile is defined by an elite combination of high visibility and operational efficiency. Unlike many growth-stage tech firms, DDOG maintains a best-in-class non-GAAP gross margin of ~81%. This profitability is anchored by a Net Revenue Retention (NRR) of ~120%, signaling that existing customers expand their spend by 20% annually. The revenue mix is healthily diversified; while marquee clients like OpenAI highlight AI dominance, the top 4,000+ enterprise customers account for nearly 90% of total revenue, insulating the firm from individual churn risks.

The emerging security and AI-native cohorts are the primary growth engines. Specifically, AI-native revenue now accounts for roughly 12% of the total mix, growing at triple-digit rates. This allows Datadog to capture higher-margin budgets, sustaining its Free Cash Flow (FCF) margins in the 26%–28% range even as it scales toward a $5B+ annual run rate.

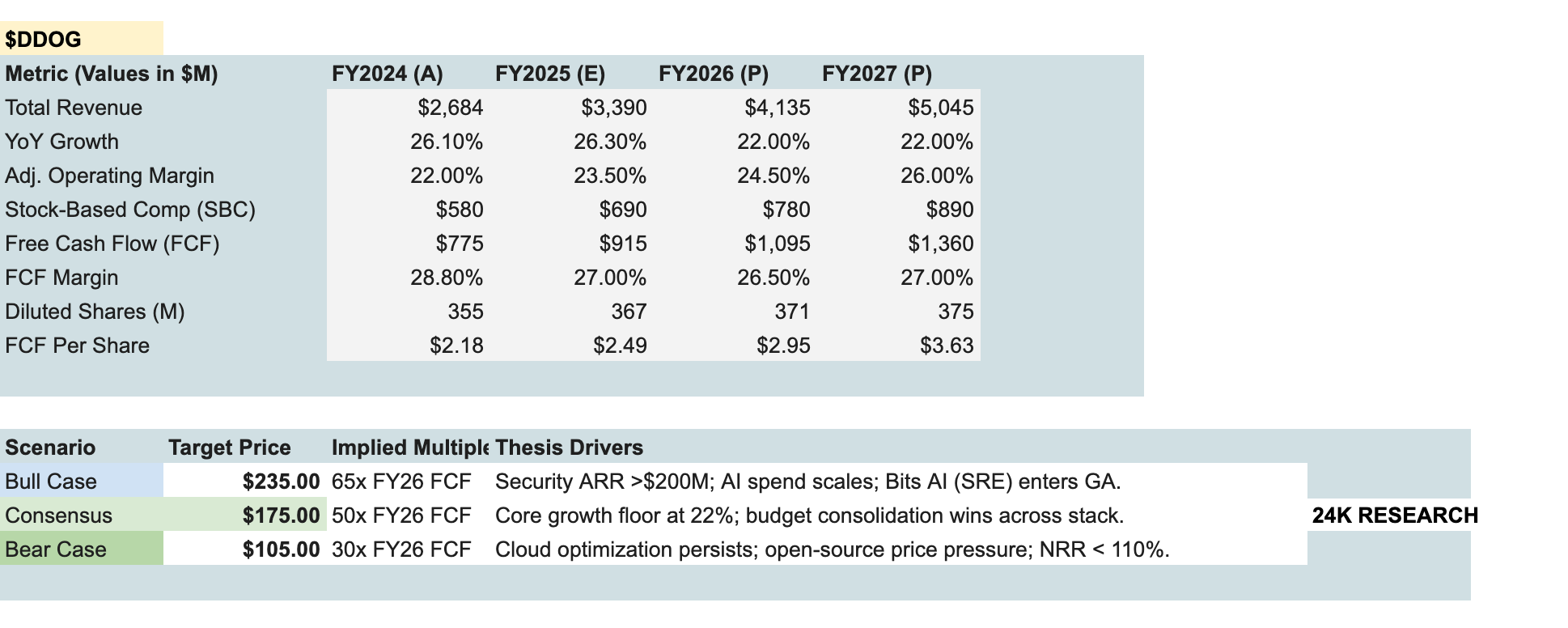

DDOG | 24K FCF Projection

Growth is driven by the “Flywheel of Complexity”. While core infrastructure is mature, the Security segment is currently growing in the mid-50% range, and AI-native customers now represent 12% of the total revenue mix.

We project a 100-150 bps annual improvement in margins as R&D and S&M expenses normalize relative to the scaling top-line. (WACC)

Our model utilizes a 8.15% discount rate, calculated using a 4.17% Risk-Free Rate (10-year Treasury) and a beta of 0.96.

Datadog remains a “cash fortress” with over $4.1B in cash and zero debt. High FCF conversion is sustained by strong deferred revenue and minimal capital expenditure requirements, with CapEx near 3% of revenue. (Conversion)

Key Partners & Ecosystem

Source: DataDog Investor Presentation 2025 Q4

Datadog’s competitive moat is reinforced by its Marketplace and Cloud Alliances.

Deep co-sell agreements with AWS, Microsoft Azure, and Google Cloud. Organizations often use cloud marketplace credits to purchase Datadog, making it a frictionless line item.

Premier partners like RapDev, AllCloud, and MegazoneCloud act as outsourced sales forces, specializing in migrating enterprise workloads to the Datadog stack.

Strategic investments in and partnerships with companies like LangChain (Oct 2025) and Chainguard (Apr 2025) ensure Datadog remains at the forefront of AI and cloud-native security.

Outlook & Immediate Catalysts (Feb 2026)

Source: 24K Research Seeking Alpha Premium DDOG

FYI I’m no technical wizard. The technical profile seen above is currently looking like it’s shaping towards a high-conviction breakout; the opposite could totally be true…this is not financial advice…with the chart showing a potential clean move above the $125.00 psychological resistance level.

The chart reflects a tightening range that typically precedes a binary move. With Q4 Earnings (Feb 10) and Investor Day (Feb 12) back-to-back, the market is pricing in a massive implied move. A 4% revenue beat would likely launch the stock toward the $138.61 52-week high, while the Investor Day serves as the fundamental justification for multiple expansion.

The recent upgrade to $160–$180 price targets suggests that analysts are betting on Bits AI and the Security roadmap to fundamentally re-rate the stock from a “Monitoring Tool” to an “AI Infrastructure Platform”. Potentially front running the events.

Key Risks

Despite the bullish momentum, we remain net-realists about the following headwinds.

Morgan Stanley has flagged 2026 as a potentially risky guidance year if the company remains too conservative regarding OpenAI’s contribution.

Palo Alto Networks (via Chronosphere) and open-source alternatives like OpenObserve are aggressively marketing 60–90% cost savings to displace Datadog in high-volume environments.

Trading at a significant premium to peers, the stock remains sensitive to any “budget optimization” narratives from large enterprise CFOs.

Conclusion

Datadog is essentially the Tax Collector of technical complexity. While the valuation is not “cheap,” the company’s ability to generate 26%+ FCF margins while leading the AI observability race makes it an essential long-term anchor. The upcoming Feb 12 Investor Day likely serves as the pivot point where Datadog proves it is no longer just a monitoring tool, but a foundational security and AI infrastructure platform. We remain neutral-slightly bullish heading into February, viewing the $131 level as a launchpad for a re-rating toward our $175 Consensus target.

24K Research, Investment Disclosure

Personal Interest & Disclaimer: As of January 22, 2026, the author maintains a net neutral to slightly long actively managed position in Datadog (DDOG). This report is for informational and educational purposes only, prepared as part of a senior-level academic finance project, and does not constitute professional investment, legal, or tax advice. All investments involve risk, including the loss of principal; readers should perform independent due diligence before making financial decisions. Forward-looking statements and Free Cash Flow (FCF) projections are based on market data available at the time of writing and are subject to significant uncertainties; actual results may differ materially from those projected. All data is provided “as is” from public filings and third-party sources, and 24K Research Corp does not guarantee the completeness or timeliness of the information presented.

Reference Sources

Earnings & Guidance: Datadog Investor Relations - Official confirmation of February 10, 2026, for Q4 earnings and current revenue trajectory.

Analyst Re-rating: Nasdaq / Fintel - Details on the Stifel upgrade to “Buy” on Jan 22, 2026, with the $160 price target.

Institutional Insights: Simply Wall St - Consensus estimates and the 32.5% projected earnings growth rate.

Product Roadmap: Datadog News - Launch details for Bits AI SRE Agent (Dec 2025) and the 1,000+ integration milestone.

Market Performance: Macrotrends - Historical price data and 52-week range verification.