Carvana Report - October Update

2025-10-11

Price: $329.24 │ Mkt Cap: $71.8B │ Short Interest: 9.5% │ 52W Range: $148 – $413

View: Slightly Bearish / Cautious

Focus: Insider selling, financing fragility, and macro sensitivity

Preface

CVNA 0.00%↑ Carvana’s story has always lived at the edge of growth, mystery and overextension. It’s one of those models that works perfectly, until liquidity doesn’t. After a euphoric 18-month run and a refinancing lifeline, the stock now sits at the confluence of strong technical support and visible structural fatigue.

We’ve revisited our earlier short-thesis as CVNA consolidates near the 100-day and 200-day averages, the inflection zone between “just a pullback” and the start of another unravel. What happens next depends less on used car demand and more on credit availability, consumer health, and how long the Fed keeps the liquidity door cracked open.

Source: Digital Trends

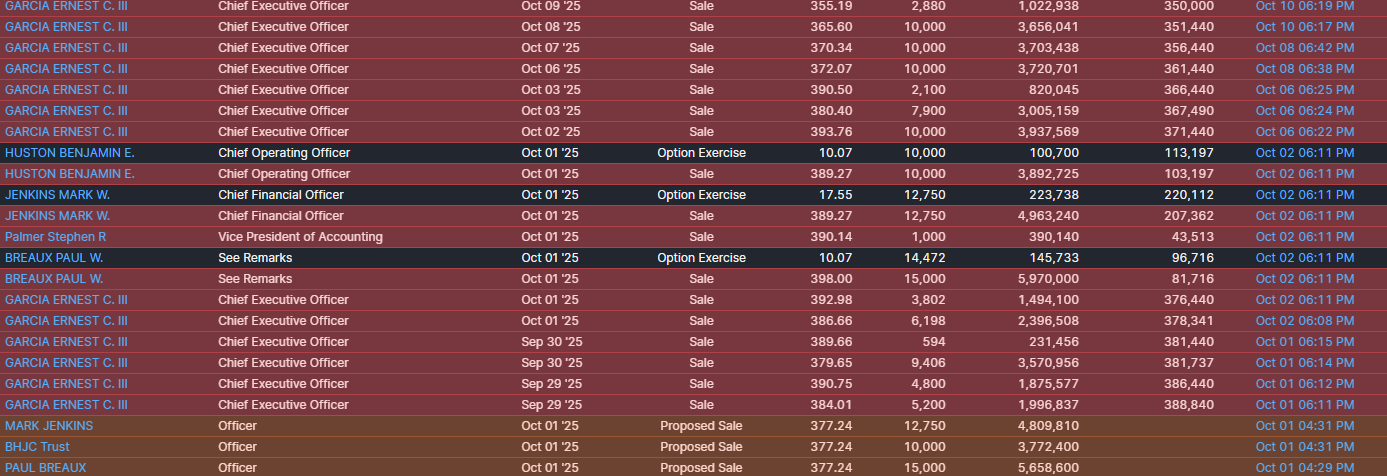

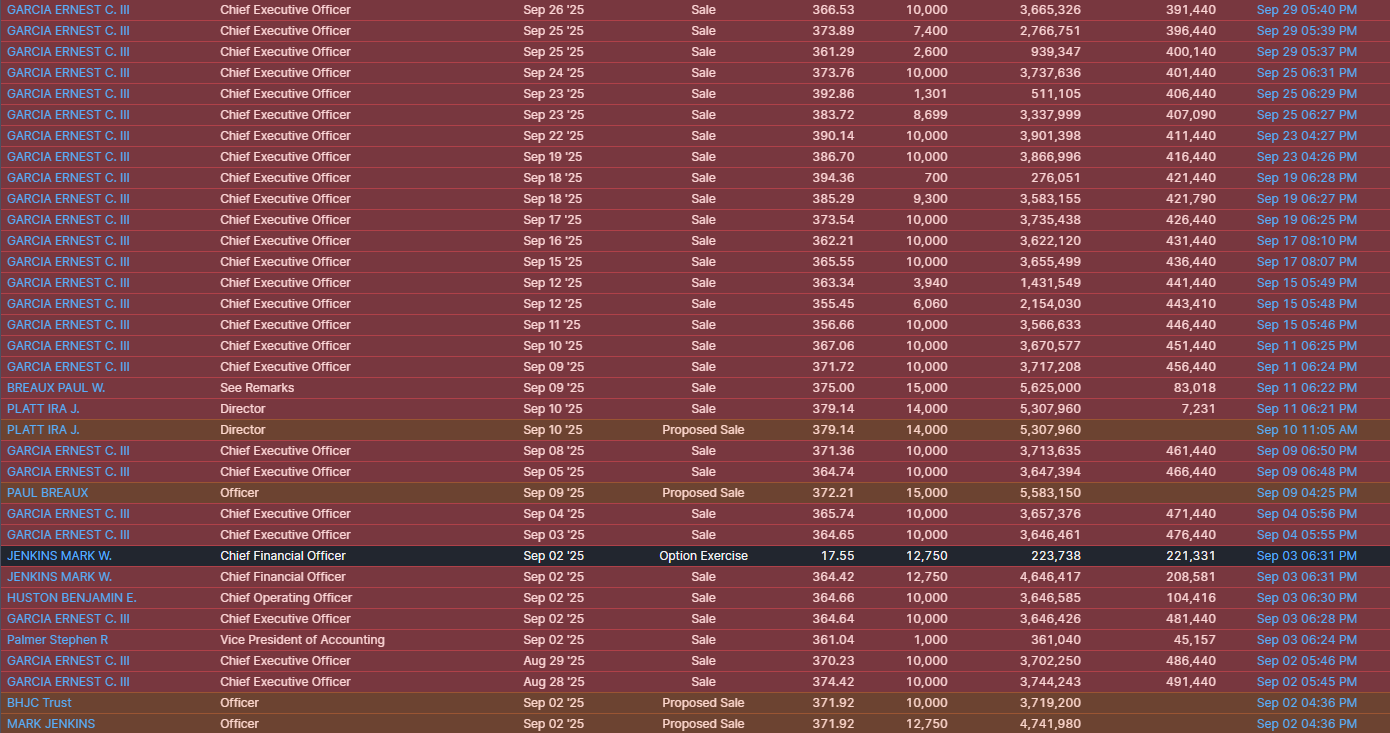

Insider Behavior: Relentless Distribution

Insider activity has been clear and consistent through late summer and early fall. The selling has been led almost entirely by founder and CEO Ernest Garcia III, joined by the COO, CFO, and multiple senior officers. Every sale in recent weeks has landed between roughly 355 and 395 dollars, executed in near-daily blocks of ten thousand shares or more. Across September and October alone…. over thirty filings were logged, none of which were paired with insider buying or equity accumulation. This is not a token rebalancing or scheduled diversification pattern. It reflects active, discretionary exits during strength.

When executives systematically sell into the company’s highest levels in two years, it carries weight beyond optics. In growth companies, conviction is often measured by insider alignment. Here, that alignment is breaking down. The behavior implies management sees current prices as generous relative to forward visibility. It also sets up a subtle but important psychological turn for the market. When leadership treats the rally as liquidity, investors eventually follow. Insider behavior, in this case, is not noise, it’s narrative confirmation that the easy phase of the comeback is over.

• Over 30 insider sales since early September led by CEO Ernest Garcia III and key executives

• No insider purchases recorded in 2025 across any senior role or board member

• Average sale prices between 355 and 395 dollars indicating consistent distribution into strength

Source: Finviz Elite Carvana

Structural Model: Financing Heavy, Top Loaded

Carvana’s operational recovery looks sharp on the surface but fragile in structure. After its 2023 debt restructuring, the company has posted margin improvement and resumed positive cash flow. Beneath that, however, the balance sheet shows a deepening reliance on financing and securitization to keep the wheel turning. Accounts receivable and finance receivables have expanded faster than unit sales, a clear sign that growth is being underwritten more by credit than by pure demand. Much of this credit risk sits with affiliated entities like Bridgecrest and GO Financial, which operate inside the same ecosystem, recycling liquidity back into Carvana’s retail arm.

This closed-loop financing offers flexibility but hides concentration risk. It smooths optics when funding is easy but can reverse violently if spreads widen or consumer credit tightens. The capital stack remains layered with secured notes and asset-backed facilities, more akin to a high-beta fintech than an auto retailer. Funding costs have come down and the securitization window has reopened, helping margins hold up in Q2 and Q3. Yet the improvement remains conditional on macro tailwinds. In a sustained high-rate environment, this model becomes top-heavy quickly…impressive when it works, unforgiving when it doesn’t.

• Accounts and finance receivables up more than 25 percent year over year against flat unit growth

• Affiliate lenders Bridgecrest and GO Financial provide internal funding covering most credit exposure

• Secured and asset-backed debt exceeds 7 billion dollars creating sensitivity to funding costs

Consumer Macro: The Hidden Weak Link

The underlying consumer data paints a more fragile picture than the share price suggests. Subprime auto defaults are ticking higher again, reflecting pressure in the lower-income segments that anchor Carvana’s customer base. Revolving credit balances have hit record highs, and the cost of financing a used car remains elevated despite nominal wage growth. The Federal Reserve’s higher-for-longer stance continues to suppress affordability. These are not abstract metrics — they feed directly into Carvana’s credit risk and loan recovery cycle.

At the same time, the job market is softening around the edges. Part-time employment is climbing, job openings are easing, and overtime hours have rolled over in retail and logistics…. the same sectors feeding Carvana’s buyer funnel. If consumer confidence dips or financing availability tightens, demand elasticity here can turn violent. Carvana’s recent strength rests less on sustained consumption and more on market tolerance for risk. In a tightening cycle, that tolerance thins fast. The consumer remains the quiet fault line beneath the entire story.

• Subprime auto loan delinquencies up over 15 percent year over year in latest industry data

• Revolving credit balances at record highs above 1.3 trillion dollars compressing affordability

• Used vehicle payments now exceed 9 percent of median monthly income for Carvana’s target buyers

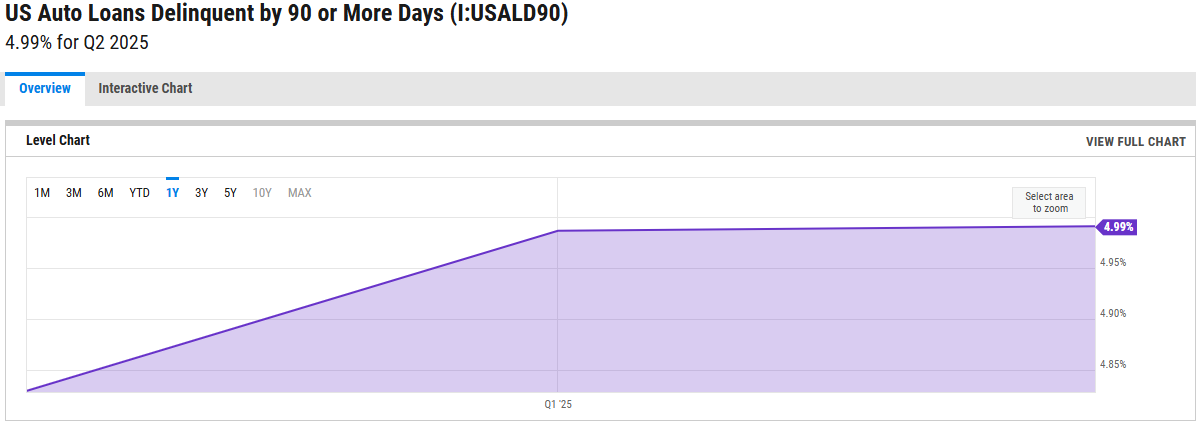

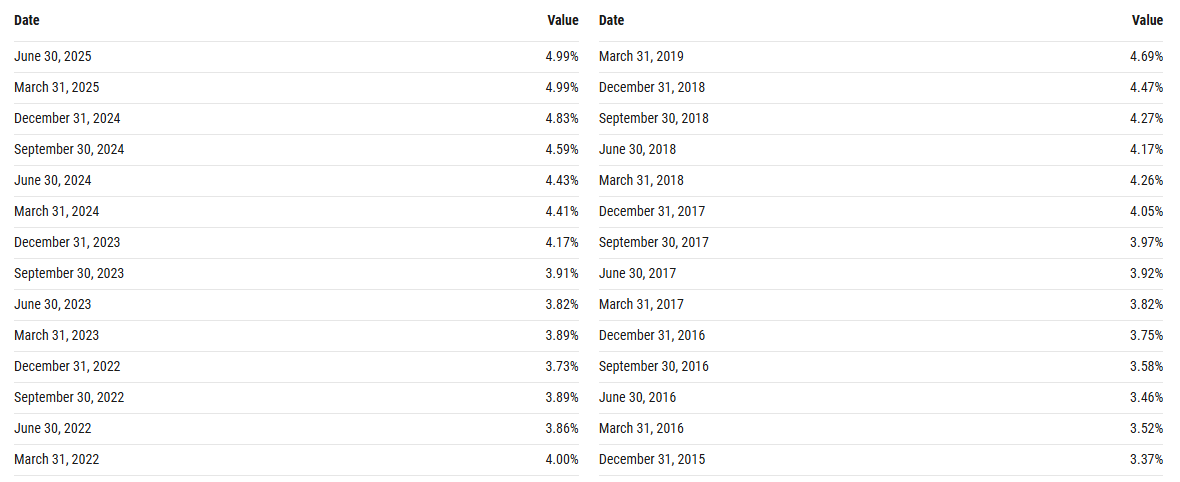

US Auto Loan Delinquencies Hit 5-Year Highs….now at 4.99%, matching pre-pandemic stress levels. For lenders and used car dealers like CVNA, this signals rising credit risk, tightening demand, and potential margin pressure ahead.

Source: YCharts US Auto Loans Deliquent by 90D+

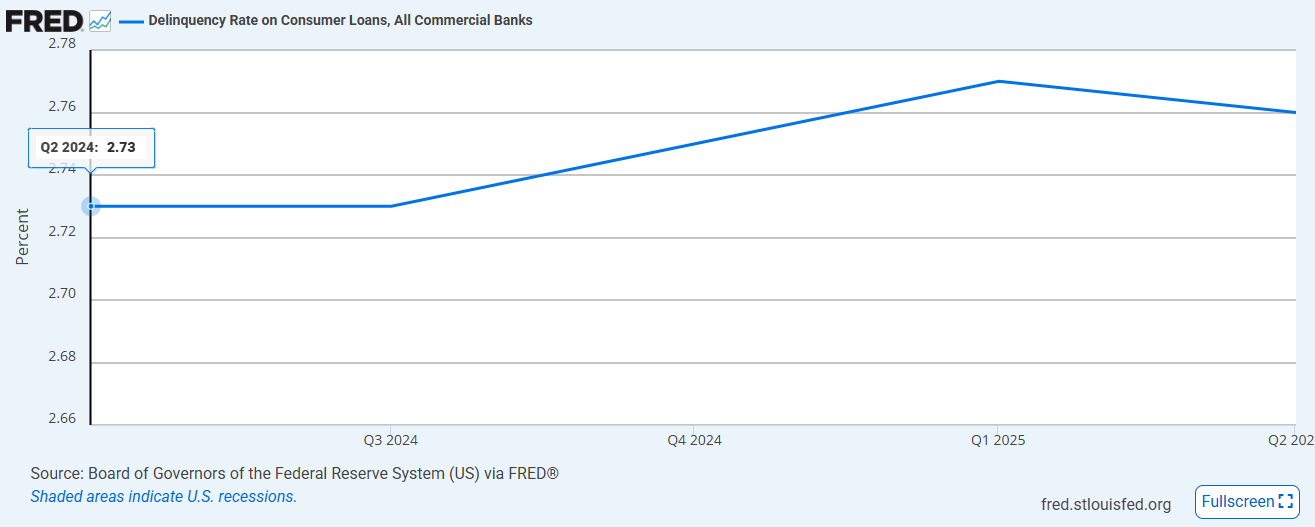

Consumer loan delinquencies have quietly climbed through late 2024 into early 2025, reaching 2.75%, their highest level since pre-pandemic normalization. While the absolute rate appears modest, the directional trend reflects tightening consumer balance sheets and rising strain across lower-income borrowers.

For a financing-dependent model like Carvana’s, even a mild uptick in delinquencies can compress loan resale margins and increase funding costs. The company’s core buyer base; credit-sensitive and rate-exposed, feels the pinch first. As consumer credit quality erodes, so does the stability of the very engine that drives Carvana’s transaction flow.

Source: FRED Delinquency Rate on Consumer Loans

Technical Picture

Carvana broke down from the 370 level, confirming exhaustion after a sharp recovery leg. The stock now trades near 329, holding just above a heavy volume shelf and initial support. Price action remains heavy, with lower highs forming since early September.

The 200-day moving average sits around 274, the next clear level if volatility persists and liquidity conditions remain tight. Momentum has softened further with RSI trending lower, while volume profile data shows a thin liquidity zone below 300, raising the probability of a fast move lower if that level breaks.

Key Data Points

• Forward EPS 5.39 and forward P/E 81.1 (Finviz)

• Market capitalization approximately 71.8 billion dollars

• Short interest around 9 percent of float, roughly 12 million shares

• Affiliate lenders Bridgecrest and GO Financial provide internal financing exposure

• Credit delinquencies up roughly 2 to 3 percent year over year across subprime segments

Carvana has broken below its short and intermediate moving averages, confirming near-term trend deterioration. The 20-day and 50-day averages have both rolled over, signaling loss of momentum after months of extended strength. Price remains below the 100-day, which now acts as resistance near 340, while the 200-day sits lower around 274 and represents the next structural test if the current support fails.

The zone between 315 and 320 marks immediate support, defined by a prior high-volume base and the lower edge of the summer consolidation range. A sustained break below 300 would expose a thin liquidity pocket, where limited volume history could accelerate downside toward the 274 region. RSI continues to drift lower, and the risk profile tilts toward further weakness if the stock cannot reclaim the 100-day moving average with conviction.

Key Levels to Watch

• Resistance: 340 (100-day moving average)

• Support: 315–320 (current shelf)

• Breakdown trigger: 300 (volume gap)

• Structural retest zone: 274 (200-day moving average)

CVNA broke below its key short and mid-term moving averages, confirming trend fatigue. Price now tests the 329 shelf with a clear air pocket below 300…. A failure, unexpected news like Friday or continued tightening here likely accelerates toward the 200-day near 274, where the next major support sits. Also worth noting the stock remains about 122% above its 52-week low of around $148, leaving room for further downside if support fails.

Source: Seeking Alpha Premium

Source: Seeking Alpha Premium

The histogram reflects weekly volume density, showing where most of the trading has taken place. There is a clear concentration of volume between 340 and 370, marking a strong supply zone where sellers have been active for months. That range now serves as resistance, with limited volume support below until around 300 to 310.

Below that, the histogram thins out sharply, creating a liquidity gap that could trigger a faster move lower if 300 fails. The next meaningful volume level is near 274, which aligns with the 200-day moving average and stands out as the next logical area for a retest if the trend weakens further. Volume continues to confirm what price already suggests the base has softened and the lower range is exposed.

Conclusion

Carvana remains one of the more fascinating battlegrounds in the market. The operational turnaround is real enough to merit attention, yet the foundation still leans heavily on leverage and sentiment. The stock’s move below key averages signals exhaustion in what was an extended run, and for now it’s settling into a zone that will test both conviction and liquidity. The insider behavior through September and October says more than any earnings call could…..management continues to distribute into strength while the market holds its breath for the next data point.

At current levels around 329, the stock sits meaningfully off highs but still well above any fundamental anchor. The structure of the chart suggests that if 300 gives way, the 200-day near 274 becomes a probable destination in my opinion. Meanwhile, credit conditions and consumer health remain the quiet drivers beneath the surface. Auto credit delinquencies are rising, disposable income growth is flattening, and higher rates continue to eat into Carvana’s financing edge. The setup is no longer only momentum-driven but macro-sensitive, and that makes timing everything.

For now, we watch. The short case remains intact conceptually, especially on a failed bounce back toward the 100-day, but patience is warranted, especially with this name and the powerful backing. This is a story of execution colliding with environment; one where valuation and gravity eventually asserts itself. No position currently, but we stay alert for confirmation before pressing the trade.

Disclaimer: This content is for informational and educational purposes only and should not be considered financial advice or a recommendation to buy, sell, or hold any security. 24k Research and its affiliates may hold positions in securities mentioned but do not make any representation regarding future performance or outcomes. All opinions expressed reflect independent analysis and publicly available information believed to be reliable at the time of writing. Markets evolve, data changes, and risk remains the responsibility of each individual investor.